HAVE ENOUGH OF YOUR NEIGHBORS THROWN IN THE TOWEL SO WE CAN BOTTOM?

WEEKLY WRAP

Prefer to Listen? Audio Version is Subscriber Only*

Futures Prices Close

Overview

Grains trying to stay alive following the USDA outlook forum yesterday.

Soybeans see a nice bounce, wheat tested it's lows from November, and corn continues to trickle lower.

The outlook forum yesterday was bearish, as expected. But overall was not "more" bearish than expected. The world was expecting bearishness, so overall the report could’ve been a lot worse.

Here is a quick breakdown of the numbers.

The report wasn’t all that negative actually. These numbers are by no means bullish at all, but they could have been far worse.

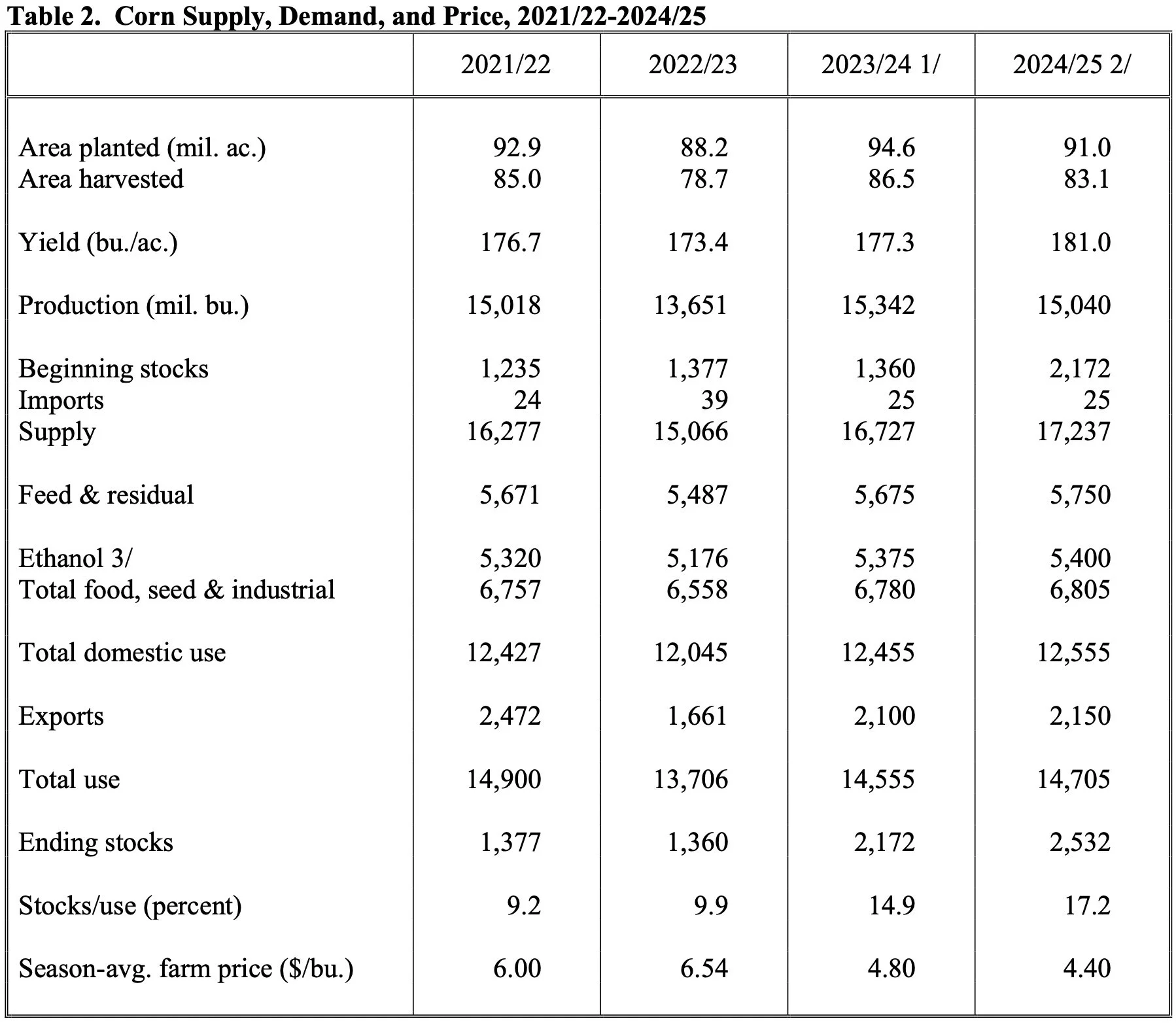

They had corn carryout at 2.5 billion. Which yes is a large number, but there was a lot of talk about a +3 billion. Historically, the USDA has been too high on their ending stocks the last 5 of 7 years.

They are starting corn yield at 181, which is well above last year's all time record yield of 177.3.

That number is possible, but especially with prices at these levels I find it hard to fathom we will be remotely close to 181. Weather would have to be perfect for this to happen, but possible I guess.

In fact, the USDA is on average 6 bushels an acre too high on their February outlook over the last 5 years. Which if happened this year, would bring us to 175.

There is a lot of talk that the 91 million acres the USDA has will be too high because of the price of corn. The thought process is that there is no way producers will throwing extra expenses at this crop or be planting extra corn. But we all know reality is that Mother Nature will have a say on actual acres, as could other agronomic factors and price movements. The recent rally in cotton is not adding more acres to anything other then cotton.

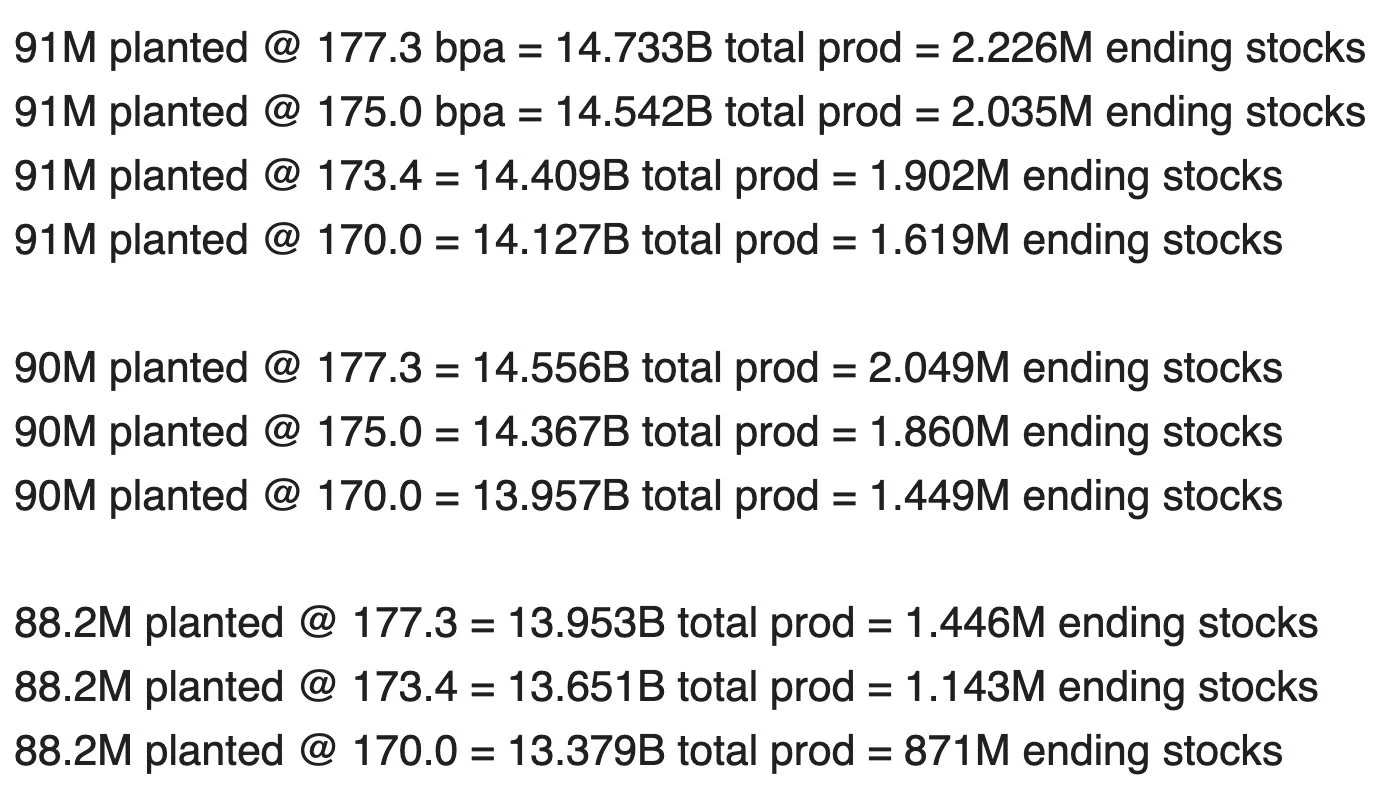

Here are some great numbers Kevin VanTrump put together. He calculated our yield and acres planted to get our potential carryout numbers.

As you can see, the less acres we get planted can have a massive effect on where our carryout comes in at.

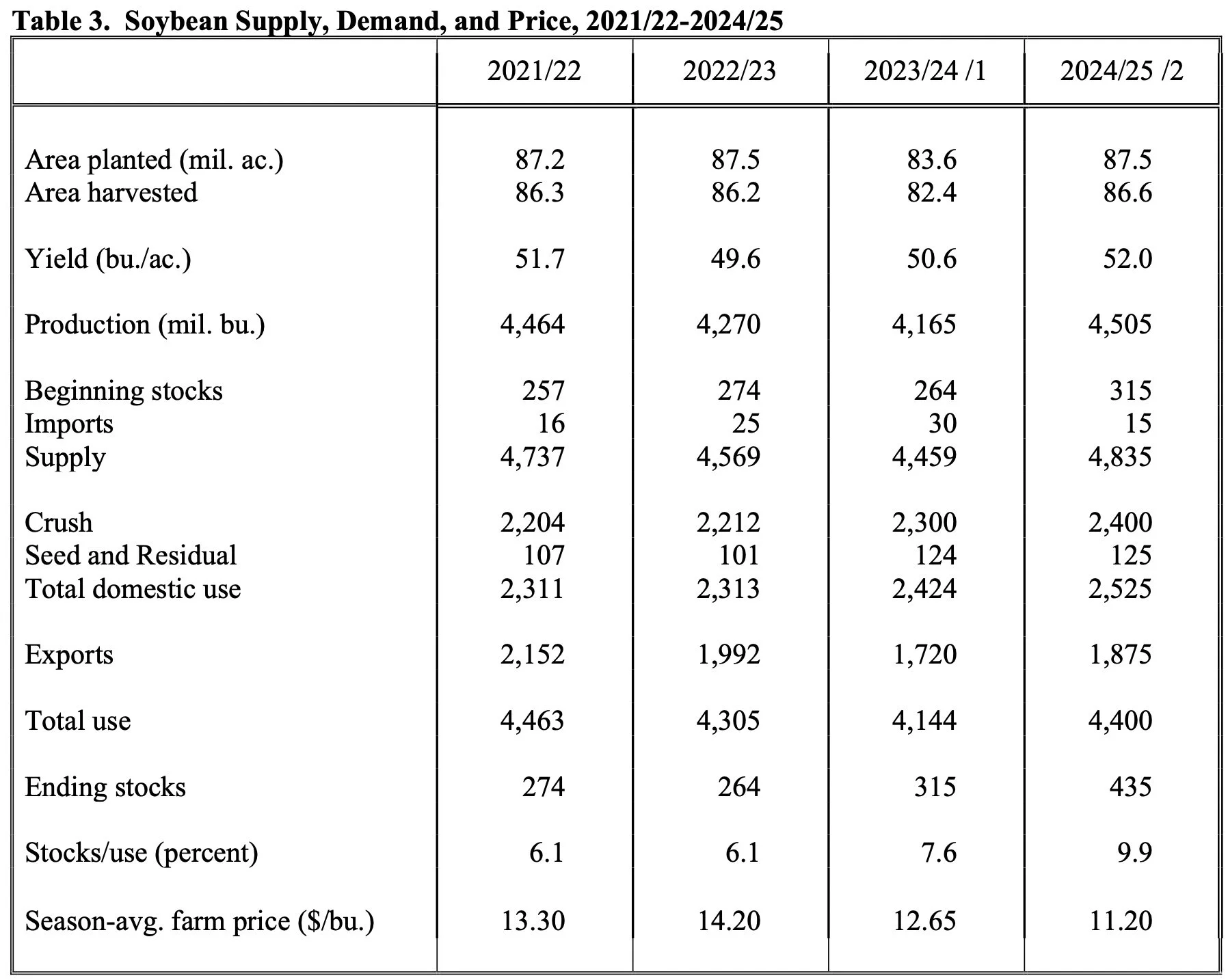

Soybean ending stocks were a lot bigger than last year. They came in at 435 vs last year's 315. The USDA has been too high on the carryout the past 12 of 16 years.

They are starting bean yield at 52. The USDA is actually surprisingly too low on the yield usually. They have been too low the past 7 of 10 years. Now this speaks volume for the demand we have in soybeans.

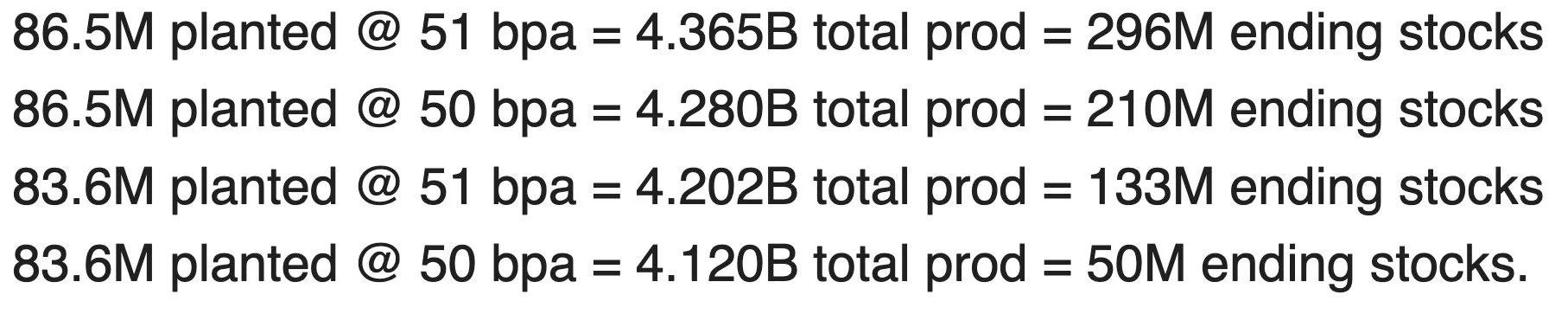

Again, here is some data Kevin VanTrump put together.

If we plant less than 87.5 million acres, things could get very tight very fast.

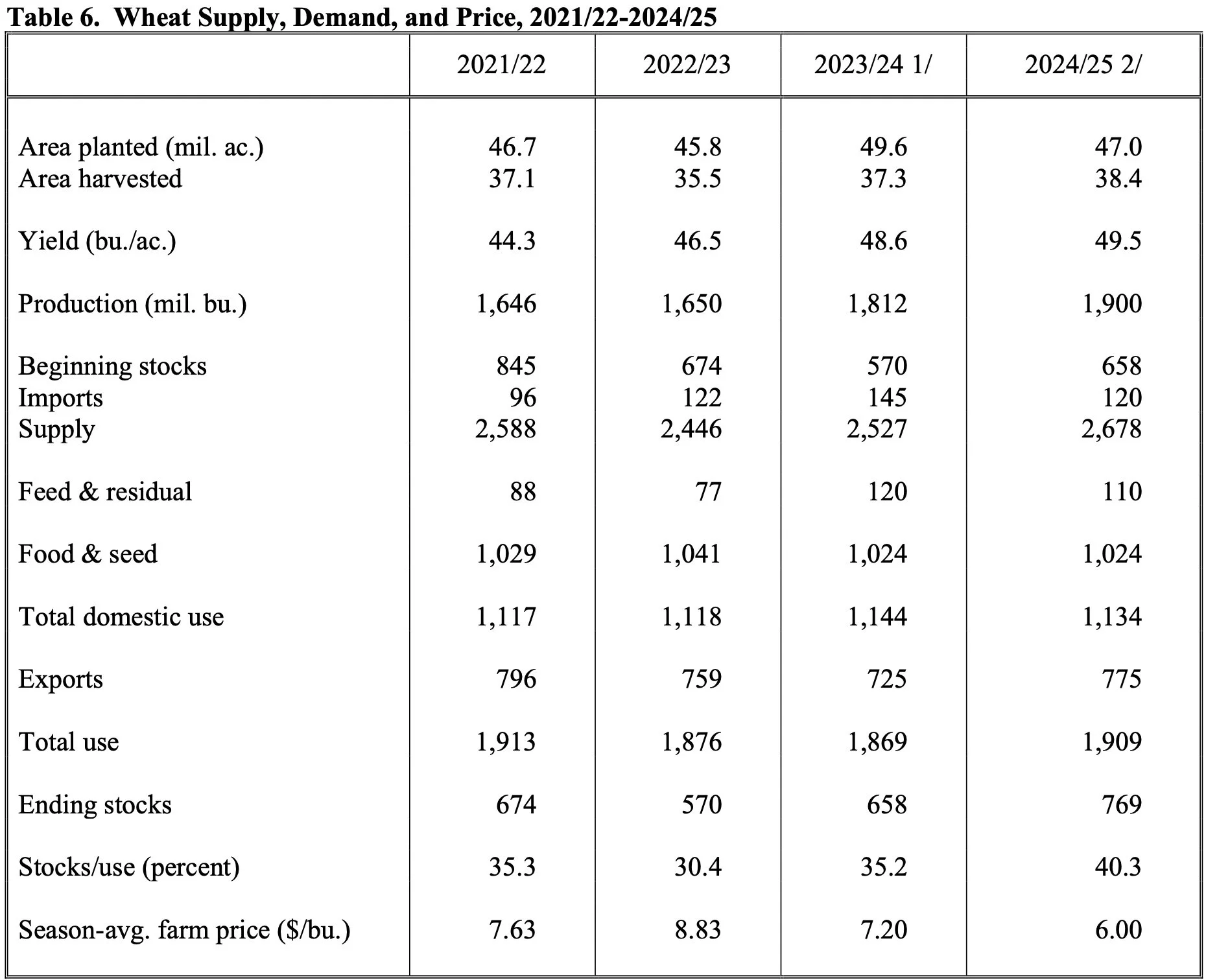

They had wheat carry out up as well, at 769 vs last year's 658.

They have budgeted in some big yields and production. What they haven’t budgeted in is the wheat acres continue to move lower across the world.

We still have several months to get the wheat crop in the bin and the market is acting like the wheat crop is in the bin, but it's not.

So the market had a negative reaction to the report, but the fact that most of the markets were actually higher today was HOPEFULLY a sign that perhaps a lot of this bearishness is already priced in.

Like we said earlier this week, this report and these numbers "should" send us straight down, but a lot of it is already priced in.

What happened the last time Brazil had a drought?

I pointed this out the other day in a soybean chart.

It took them until the last week of February to realize the damage.

Not saying the exact same thing will happen this year, as there are several different factors at play. For example, our +2.5 billion carryout in corn and Argentina expecting to have nearly double the soybean crop they had last year.

But it is interesting to note at just how long it took them to realize it last time. So who is to say something similar can’t happen this year?

Just something to watch.

Here both the corn and soybean continuous charts from 2016.

Soybeans found solid footing at the end of February. Corn chopped sideways until finding a bottom in late March.

Both rallied substantially before making their highs in June. Corn rallied +92 cents. Soybeans rallied $3.50.

Now let's jump into the rest of today's update..

Today's Main Takeaways

Corn

Corn continues to trickle lower.

We talked a lot about elevators forcing producers to exit their basis contracts yesterday. You can listen to that audio HERE.

Make sure you do your due diligence and understand exactly what your contract says as to what happens when you take an advance. Also keep in mind that one of the devils greatest tricks was convincing the world he didn’t exist. Don’t put it beneath a grain buyer to try to scare producers to sell "before it goes lower".

Below is a conversation I saw between a few highly respected people in the industry.

This is similar to what I said about not putting it beneath a buyer to sell you fear. Who is the biggest buyer in the world? China………..

The rest of this is subscriber-only. Please subscribe to keep reading and get every exclusive update & 1 on 1 marketing planning.

IN THE REST OF TODAYS UPDATE

Is China playing us like a fiddle?

When adjusted for inflation, corn is $3.00

Where did we bottom last bearish cycle?

Critical support levels to watch

Factors that could spook the funds

Risks for seeing $3 corn?

Are the markets overdue?

Is everything “fine” in Brazil?

TRY OUR DAILY UPDATES FREE

Get 1 on 1 grain marketing planning & tailored recommendations. Make this the year you beat big ag at their own game.

Want to Talk?

Our phones are open 24/7 for you guys if you ever need anything or want to discuss your operation.

Hedge Account

Interested in a hedge account? Use the link below to set up an account or shoot Jeremey a call at (605)295-3100 or Wade at (605)870-0091

Check Out Past Updates

2/15/24

BASIS CONTRACTS & USDA OUTLOOK

Read More

2/14/24

SELL OFF AHEAD OF USDA OUTLOOK: STRATEGIES TO CONSIDER

2/13/24

LA NINA, FUNDS, & USDA OUTLOOK FORUM

2/12/24

WHAT TYPE OF GARBAGE USDA OUTLOOK REPORT IS ALREADY PRICED IN?

2/9/24

RECORD SHORT FUNDS, SOUTH AMERICA, & MANAGING RISK

2/8/24

CONAB VERY FRIENDLY. USDA NOT. FULL BREAKDOWN

2/7/24

NEW LOWS IN CORN & USDA PREVIEW

2/6/24

WHAT IS EXPECTED FROM USDA & WAYS TO GET COMFORTABLE

2/5/24

STILL NO CLEAR DIRECTIONS IN THE MARKETS

2/2/24

NEW BEAN LOWS.. HOW LOW CAN CORN GO?

2/1/24

NO CONFIRMATION OF HIGHER OR LOWER PRICES IN GRAINS

1/31/24

HOW SHOULD YOU BE SETTING YOUR TARGETS?

1/30/24

OUTSIDE UP DAY IN ALL THE GRAINS

1/29/24

GEO POLITICS, CHINESE, BRAZIL, ALGOS, & BIG MONEY

1/26/24