WEEKLY NEWSLETTER

By Jeremey Frost

This is Jeremey Frost with some not so fearless grain market thoughts for www.dailymarketminute.com

How are the ag markets and grain prices divided?

Are there teams against each other when it comes to grain prices? Is it bulls against bears? Elevators against farmers? Buyers against sellers? Producers versus consumers? Is there always a winner matched with an equal loser? Do days when grain markets go up, mean that farmers won the game we call commodity markets?

If you go to a casino is it you versus the casino? If you play on the Wall Street Casino is the stock market your opponent? After all, isn't everything an equal sum game?

Do farmers who grow grain have an opponent? Is it the managed money, the funds, big money as I like to refer to them as? Is it the commercials? The big elevator ABC companies such as ADM, Bunge, and Cargill?

Are sometimes the various groups I mentioned above just as much our allies as our opponents?

Let’s take a look at some of these questions as you decide the answers. In your head as you read the above questions did you think to yourself “yes, but it’s a little more complicated than that?”

My thoughts on some of the questions. First off if on any day the price goes higher we had more buyers then we did sellers at least at that specific price correct?

A couple observations. First off when a farmer sells grain on a given day they have not committed treason have they? My answer might shock some of you and that answer is at times they have crossed a thin grey type of line and have committed treason to their operation.

I will give you an example. On Facebook aka meta grain market discussion group someone on how wide of basis ADM Silver Grove was for corn. Below is from grainbridge. You will see that the bid difference is 2.18 a bushel from the nearby versus the February cash bid.

If one has ever had a reason to invest in a bagger or build bins I think this farmer has one. As to many that are typically supplying grain that is going down the Mississippi River.

I have to admit I have never traded barges but I have traded some rail freight. I know if I owned rail freight for a few hundred bucks a car and now I could sell it for $5,000 to $20,000 a car I would sell the car back and put the grain on the ground if at all possible.

My sources tell me that in spots every 100% of the tariff is about 15 cents a bushel; so for every 1000% of tariff, it is about 1.50 a bushel. I have seen reports of things trading over 3500% of tariff. Ouch someone is making a killing.

My question is do you think that any elevator is going to take it on the chin with the barge freight going crazy? My guess is it is going to get passed down to the farmers that commit treason and sell this ugly basis.

If you are a farmer and are forced to sell this ugly basis, realize that is the reason you have a big gap versus your neighbor who didn’t sell the wide basis.

Elevator’s and commercial’s are allies most of the time, as is big money when the markets are going higher. But keep in mind that allies are not always on the same team. They are not teammates to the farmers; they can be great business partners. But ask yourself if you know any grain buyers that get bonus checks for paying more than the competition.

In not so simple terms the opponent of farmers is anyone who sells grain or supplies grain on a given day, but keep in mind this is something that needs to happen or we lose demand and every farmer loses.

Farmers do have a choice to be proactive and stay out of the giving it away scenarios such as those that are selling corn for $2.18 less a bushel today then if they contracted it for February delivery.

So to answer the opening question, how are the ag markets and prices divided? It changes minute by minute, day by day, everyone wants what is best for the farmer, until they find something that is more appealing to themselves.

The harsh reality is very few always want to do what is right for the farmer. The only way to always do what is right for the farmer includes having no other motivation other than trying to be the best at what one does thus having farmers come back to do business with one. Separating the incentive with the result.

What drives www.dailymarketminute.com is to give the best advice possible so that I can get farmers the results they need in their operation; so that they continue to do business with me. The reason we are offering 50% off using the code word GRAIN is that we believe that we will earn repeat business via helping farmers. I believe most farmers are the most loyal customers in the world and if you do right by them they will return the favor.

If you are not reading up on the markets and are selling grain at the ugly basis levels like above do yourself a favor and find an advisor to work with. It doesn’t have to be me; there are plenty of good grain marketing newsletters out there.

One of them Roger Wright posted this the other day on https://www.wrightonthemarket.com

Marketing Questions from Clients.

Roger, do you think the carry to March from Dec (corn) will get more than 7-8 cents as we work into harvest? Just curious if I should put an order in to roll my HTA's to March at 8 cents. Looking at spread chart between these two months it doesn't look like we have gotten any more than 8 cents of carry since before 2021. I am expecting a better basis in March -July. Thanks!

Get your order placed to roll from Dec to March at 8 cents. That is a heads-up question. I have been waiting for ten months for that spread to get to 9¾. I have been distracted in recent weeks and had not been thinking about it as often as I should have.

It will take an incredibly bearish crop production report and poor demand on the S&D on October 12th to get that spread to 10. I see very little (5%) chance that will happen.

As you noted, the spread was 8 cent maximum the first week of August (see chart below). Normally, as we approach harvest with normal yields, that spread (return to carry) will easily get to 11 or 12 cents and sometimes 13+ with good yields and relatively large carry-in. The USDA informed us on September 30th we do not have a large carry-in and I just do not see yields going to 178 bushels this year. Even if that 178 yield was reported, I doubt that spread will get to 10.

The market is telling us the Dec to March spread is not going to be 10 to 13 this year. The carry from March to May is just one cent and July corn is 5½ under the May… it is inverted. The market is telling us it will not pay anyone to store corn from March to July, so why would the market pay more than 8 cents to get from harvest to March?

The return to storage after December will not pay, but you are correct to expect substantial basis improvement into next spring.

Marketing question: I have about 2/3 of my soybeans sold at a price I am very happy with. Well above 14 dollars and it locked in a good profit for me. My question is on the other 1/3, am I better off to sell at this lower price and buy them back using call options, or pay the 5 cents a month storage at the elevator? Grain bin storage is not an option. Thank you

Of those two choices, I would pay storage until mid-December to capture the basis appreciation from harvest to December and then switch to a July call option. Make sure your merchandiser will let you go from storage to sell beans and buy a call option before you do anything. Let’s look at the math to store versus sell now & buy a call.

If cash beans delivered now are worth $13.50 and you are paying 5% interest on an operating loan, 5% times $13.50 = 67½ cents interest per bushel per year, which is 5.6 cents a month per bushel. Add the 5 cents a month commercial storage fee and your opportunity cost to own those beans is 10.6 cents per bushel per month, which is 26½ cents until the third week of December. That is a fixed cost. You will have to pay that cost whether the bean futures price goes up or down.

By the third week of December, the cash bean price will have gained 10 cents of carry (January futures price is 10 cents above November futures price) plus basis appreciation of 30 to 50 cents. Let’s say 40 cents. So, the net cash bean price to you on December 23rd will be 23½ cents more (50 cents carry & basis gain minus 26½ cents ownership cost) plus or minus the futures price change.

If you sell the beans now for $13.50 and take 55 cents of that money to buy an at-the-money January $13.80 call, you will maintain a long position in the bean futures market with the risk of loss limited to 55 cents.

If January beans are at $13.80 on expiration day (December 23rd):

The basis and carry would gain 23½ cents with no futures gain if stored.

The call option would expire worthless, losing 55 cents.

If January beans are at $14.00 on expiration day:

The basis and carry would gain 23½ cents plus 20 cents futures gain = 43½ cents if stored.

The call option would be worth 20 cents, losing 35 cents.

If January beans are at $15.00 on expiration day:

The basis and carry would gain 23½ cents plus $1.20 futures gain = $1.43½ gain if stored.

The call option would be worth $1.20, net profit of 65 cents (sell at $1.20 minus 55 cent cost).

If January beans are at $16.00 on expiration day:

The basis and carry would gain 23½ cents plus futures gain of $2.20 = $2.43½ gain if stored.

The call option will be worth $2.20 cents, net profit of $1.65.

If January beans are at $13.00 on expiration day:

The basis & carry would gain 23½ cents minus futures loss of 80 cents = 53½ cent loss if stored.

The call option will be worth nothing, losing 55 cents.

If January beans are at $12.00 on expiration day:

The basis and carry would gain 23½ cents minus futures loss of $1.80 = $1.56½ loss.

The call option will be worth nothing, losing 55 cents.

You did not ask, but I suggest you consider storing for two months then switch to a July basis contract or sell the cash beans in December and buy futures. Either of them will net you 10 cents more a month than storing with the same market risk.

The easy money is the basis appreciation from harvest to post harvest plus the 10 cents carry to January. Right now, there is another 20 cents of carry from January to July, but basis would have to firm 31 cents to breakeven on the storage.

Of course, if bean futures go up $3 by May or June, one would think storage would pay. Nope.

You would have $13.50 tied up waiting to make $3 and paying 10.6 cents per month to boot. You can sell the cash beans when storing no longer pays and use $1 as margin money to buy beans in the July futures.

Which is better: turning $13.50 into $17.50 and paying 10.6 cents a month to do it

or

turning $1.00 into $4 and paying interest on $1, a half cent a month?

If you do a basis contract in December, you probably would get 70% of the cash value and tie up $4 to earn another $3. Marketing decisions need to include money management.”

He also posted this recently which should serve as a reminder that elevators are not always on the same team as farmers. They can be, but not all are and most of the time they are allies until they find something that better suits themselves.

https://www.wrightonthemarket.com/post/cargill-does-not-make-mistakes

Cargill Does Not Make Mistakes

“Roger Scheiderer has been a client of mine for 36 years. He farms near Plain City, Ohio just northwest of Columbus. In 1986, he got into the milk hauling business, which migrated into the hopper-bottom over-the-road transport business about 20 years ago.

Roger is everybody’s friend and easy to talk to. Consequently, many members of the area’s prominent Mennonite population stop in to discuss everything and often ask Roger for advice about more “worldly” things.

On an early September afternoon in 1999 or so, Roger called me. The conversation went like this:

“Joshua stopped in here to ask me a question about marketing his beans. I told him you were the guy to talk to, so I am going to hand the phone to Joshua.”

Joshua explained that he was going to harvest 40,000+ bushels of soybeans in the next few weeks. He recalled Roger Scheiderer had told him months ago there was a way he could deliver his beans, get most of his money, and still benefit if the price of soybeans went higher. Was that true?

I said yes, that was a “basis contract.” I explained that the final cash price paid for soybeans was the futures price plus or minus the basis.

I told him to think of the futures price as the world price for beans based upon the world supply-and-demand. Also, think of the basis as the local price for soybeans reflecting the local supply-and-demand compared to the world supply-and-demand.

If a community produced more beans than the community needed, those extra beans needed to be transported out of the community into the world marketplace. That transportation had a cost, and that cost came off the price of the beans, which resulted in the local price being below the futures (world) price. That price difference resulted in what was called a “negative basis.” An area with a negative bean basis is “a bean surplus area.”

On the other hand, if a community used more beans than the community produced, it needed to attract beans from the world marketplace into the local community, and that transportation cost money. Therefore, the price of soybeans within the community would be above the world price, and that resulted in what was a called “positive basis.” An area with a positive bean basis is “a bean deficit area.”

Regardless of the basis, one way to receive money for the beans and still have an opportunity to benefit from price appreciation was to deliver the beans. At that time, he could cash out the beans for full value and buy futures. That would tie up 5% of the bean income, or he could leave 30% of the value of the beans at the elevator and have the elevator buy futures for him. Such a transaction was called a “basis contract.” He could pick the day he wanted to lock in the futures price. At that time the elevator would pay him the 30% he had left at the elevator plus or minus whatever the futures market change had been from the date the basis contract was established and when the futures price was fixed on his order.

Joshua said he would not trade futures, so he would do a basis contract. He asked if I would help him set it up with Cargill. I said sure. But I told him that if the price of beans went down more than 30% after he received his 70% cash advance, he would owe Cargill money. He said that made sense and was no problem.

“Where do you want to deliver the beans?”

Joshua said, “Sidney Cargill.”

I got Cargill’s merchandiser on the phone and explainedJoshua and I were calling to establish a basis contract for October delivery of 40,000 bushels of soybeans. The basis was 40 under the November, which meant the basis contract would have to be priced or rolled to a deferred futures month by the next-to-last business day of October. I confirmed that Cargill would advance 70% of the value of the beans as of the day the beans were delivered. Cargill’s merchandiser said he would send a contract to Joshua to sign and return. The deal was done.

I told Joshua to be sure to read the all the fine print on the contract and double check that it stated 40 under the November, which would probably be stated as -40X.

A week later, Roger called me and said Joshua wanted to talk to me again. Joshua said he got the basis contract, and it said the basis was +40X, not -40X.

Holy cow! The difference between 40 over and 40 under is 80 cents on 40,000 bushels. That is $32,000! In 1999, that was real money! That was a year’s wages at a local factory for a 40-hour week!

I said he had two choices: Call Cargill, and tell them they made a mistake. They will send a corrected copy or sign the contract, then return it and wait for them to contact him to tell him they made a mistake. If Cargill did not catch the mistake before they wrote the check, they would most certainly catch the mistake when they did write the check. In any case, I told Joshua not to think for one minute he would be paid 40 over the November for the beans. I sensed the choice of to call or not to call Cargill was a big stress for him.

Four days later, Joshua called me to say he could not sleep at night. He was going to call Cargill and tell them they made a mistake. I said, “OK. It does not matter, Joshua. They were never going to pay you 40 over the November anyway.”

Ten minutes later, Joshua called me back. His voice sounded as if he was on an LSD trip.

He explained to me he told the merchandiser about the mistake on the contract, stating 40 over instead or 40 under.

The merchandiser told Joshua in a very arrogant tone of voice, “Cargill does not make mistakes!”

Joshua went on the explain the merchandiser was highly insulted by Joshua’s insinuation that the contract should be 40 under instead of 40 over the November. After all, he was just a farmer, and he needed to stick to growing soybeans and leave the marketing to Cargill.

Joshua did not know whether to be happy or pissed-off. I assured him he would never see that $32,000.

But I was wrong; he was paid 40 over the November. As a grain market advisor, that was my most flagrant 100% wrong prediction ever.

Somewhere in the vicinity of Plain City, Ohio, to this day, there is a Mennonite farmer thinking every day he will spend eternity in Hell because he received $32,000 from Cargill that he did not deserve.

No, Ladies and Gentlemen, Cargill does not make mistakes, and don’t you forget it!”

USDA REPORT Are You Ready For It?

This week will bring the USDA WASDE report. My thoughts haven’t changed here. I think we see grains close in the green for the week and higher by the end of the month.

I look for corn to break $7.00 futures this month and most likely this week. Look for wheat to gain back all of it’s losses it had this week which is a big prediction considering CBOT wheat was off over 40 cents.

AntiTrust - Class Action Lawsuit

With recent headlines “Regulators Accuse Pesticide Makers of Inflating Prices for Farmers” in the Wall Street Journal I have had a few farmers ask me about some specialty grains with some of the recent acquisitions and mergers that have happened. I have been in contact with an AntiTrust and Class Action Firm that has had a large amount of success in the ag industry. Please send me your contact info if you would like more information or be included in a possible class action lawsuit for AntiTrust and price fixing for some of the speciality grains. (Email me at jfrost@banghartproperties.com)

Free Grain Marketing Plans

We are presently offering free grain marketing plans. Fill out a questionnaire and we will send you back a grain marketing plan. Send me your email address and I will send you over the questionnaire. You can text me at 605-295-3100 or email me at jfrost@banghartproperties.com

Millet Market

I am waiving the yellow flag for the millet market. As it has stalled out a bit. I still think it has upside but we need to see some demand as coverage has slowed down buying interest.

Sunflower Harvest

Sunflower harvest is running behind and the later it takes to really get going the bigger the risk of possible storms doing damage. Buyers remain patient but I still believe we are about a month away from turning back into a sellers market. The bean oil chart looks to be ready to breakout to the upside as well. Look for the buyers that have had no bids (no antitrust happening right?) to start all coming into the marketing attempting to buy. Farmers do your job and run the price backup on them!

Why grains could be going much higher tonight

Increased conflict between Russia and Ukraine.

Conspiracy Corner

Plenty of links to Conspiracy Corner type info is listed in the zero hedge article.

Everyone knows of the Mississippi River drying up. But here is another with the Euphrates River drying up and a biblical prophecy coming to pass?

What happens if China invades Taiwan?

China planning on invading America?

China turning pills into mass destruction?

Still on a free trial? Use code: GRAIN for 50% off yearly/monthly subscriptions so you don't miss a beat. Updates sent out via email and text message

Commodities Overview by Sebastian Frost

Overview

Friday we saw an unexpectedly strong finish across the grains, given the absolute fallout in the stock and equity markets. As the Dow Jones closed Friday down -2.11% with the S&P closing down nearly -3%. A lot of the weakness we saw in the equity markets was the unemployment report. With the report suggesting that we will continue to see interest rate hikes. I'm not entirely sure why the markets saw this as such a shock, as everyone already knows interest rates will continue to rise for the time being.

Next week everyone's focus will be the October USDA supply and demand report, which is scheduled for Wednesday.

Today's Main Takeaways

Corn

Corn finished the week off higher on Friday. As we closed Friday +7 3/4 cents higher. Which was near the top of the trade, as Dec-22 corn closed nearly +12 cents off its early lows.

Crude oils week long rally has added much needed support to the market. As crude oil finished the week off a little over $4 higher, and over $11 higher on the week (+13.87%). The news that the OPEC+ is looking to cut their oil production added a boost, as they are looking to cut production by 2 million barrels a day.

Private Analyst IHS Markit lowered their 2022 U.S. corn yield estimate to 171.2 bushels per acre. This is a 1.3 bushel per acre decrease from the 172.5 bpa last month. They also lowered their total U.S. corn production estimates from 13.944 billion bushels down to 13.839 billion.

All eyes are on Wednesday’s USDA report. As it looks like most are expecting to see a small trim to the yield estimates. According to Bloomberg, they are expecting corn yield to be trimmed by 0.4 bushels per acre, down to 172.1 bpa. We will have to see just where they come in at. As most think its still too early to see any crazy cut. As for production estimates, they are looking at 13.903 billion bushels and expect carryout to drop 93 million bullish.

Brazil

According to CONAB, Brazilian farmers are expected to increase their corn planted area by 3.8% to a record 22.4 million hectares. However, full season corn planting is expected to decrease 1.5% as producers are looking to plant more soybeans.

CONAB projects Brazils corn production to raise 12.5% to a record 126.9 million metric tons.

Crop consultant Dr. Michael Cordonnier forecasts 2022-23 Brazilian production at 125.5 million metric tons.

CONAB expects corn exports to jump 21.6% to 45 MMT in 2002-23.

5-Day Change

Dec-22 Corn: +5 3/4 cents

Dec-22 Corn (6 Month)

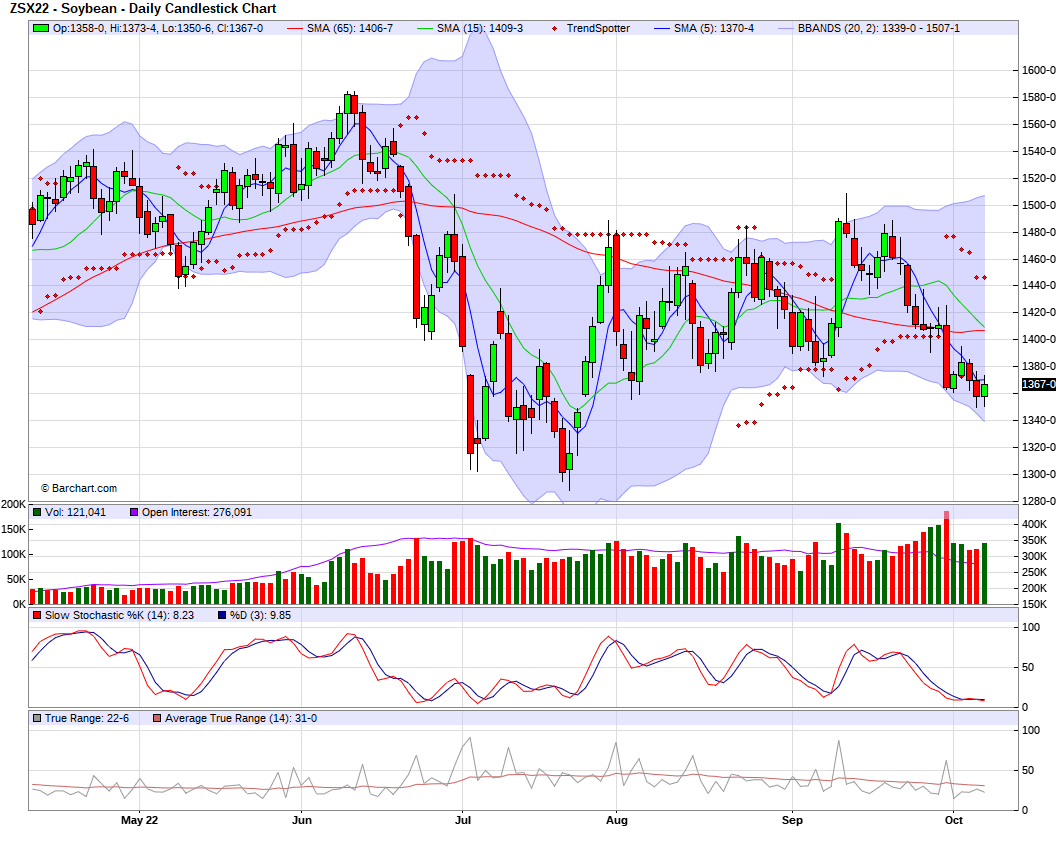

Soybeans

Soybeans ended the week off pretty firm, as we saw some bargain buying following sharp losses to start the week off. Soybeans closed Friday +9 cents higher, and well off their highs (+16 cents).

Despite the strong end to the week, the soybean charts still don't look great. Perhaps we do see some corrective buying. But soybeans are still under a lot of pressure with very weak demand as well as harvest pressure.

Soymeal remains under pressure from the strength of the dollar. We still haven’t seen in increase in Chinese demand. So its tough to justify higher prices until we do something from the demand side of the story and maybe see the dollar cool off. However, with the Argentina planting struggles due to drought, there is a chance this becomes a bigger problem and adds support to markets as the year goes on.

CONAB's Brazil 2022-23 soybean production estimates came in at 152.4 million metric tons. An increase of 21% from last year.

Private Analyst IHS Markit lowered their 2022 U.S. soybean yield estimate down to 49.9 bushels per acre. A decrease from last months 50.5 bushels per acre. Also lowering their soybean production estimate from 4.378 billion bushels to 4.327 billion.

Similar to corn, the focus for the start of next week will obviously be Wednesday’s USDA report. Reports from the field are really a mixed bag with some saying yield is higher than estimates and some saying its lower. The current forecast is at 50.5 bushels per acre. There is a chance that the USDA just leaves its estimates unchanged until they get more sufficient data. Most are suggesting we see a slight increase to last years production. As for exports, there is a pretty good chance we see exports left unchanged but we could definitely see a small cut.

Brazil

According to CONAB, Brazilian farmers are expected to increase their soybeans planted area by 3.4% to a record 42.9 million hectares.

They are forecasting 2022-23 Brazilian soybean crop at a record 152.4 million metric tons.

Crop consultant Dr. Michael Cordonnier forecasts 2022-23 Brazilian production at 151 million metric tons.

CONAB forecasts soybean exports to jump 22.5% to a record 95.9 MMT for 2022-23.

5-Day Change

Nov-22 Beans: +2 1/4 cents

Nov-22 Soybeans (6 Month)

Wheat

Wheat ended the week off slightly higher at Fridays close. But showed more weakness as the day went went on. With wheat closing near the bottom of its trade range. With Chicago wheat closing over -16 cents off its highs, KC -16 cents off its highs, and MPLS -14 cents off its highs.

Last week we saw impressive gains across the board for wheat, as they ended +30-40 cents higher for the week. However, the losses we incurred this week have erased most of the gains we saw last week.

Wheat continues to see pressure from as the U.S. dollar remains strong and as overall demand remains weak.

Following the news last week, where we saw the vote to annex four regions in Ukraine. We haven’t got much of an update, as the news surrounding the Russia and Ukraine situation has remained fairly quiet. Overall the situation remains a wild card.

As for next week's report, it looks like most are expecting to see a somewhat slightly tighter balance sheet for the U.S. come next Wednesday. Everyone already knows we will see U.S. production trimmed at least a little bit. One of the larger question marks is just how much exports will be lowered. It's looking like most are assuming we see U.S. wheat ending stocks to be lowered to 600 million bushels or lower.

All wheat classes were lower on the week. With Dec MPLS wheat posting its largest weekly percentage decline since the middle of July.

5-Day Changes

Dec-22 Chicago: -41 1/4 cents (Last week +41 cents)

Dec-22 KC: -22 3/4 cents (Last week +41 cents)

Dec-22 MPLS: -14 cents (Last week +32 3/4 cents)

Dec-22 Chicago Wheat (6 month)

Dec-22 KC Wheat (6 month)

Dec-22 MPLS Wheat (6 month)

Crude Oil

Crude oil saw a massive rally to end the week Friday, adding on top of its week long gains. Crude oil closed Friday up $4.20 (+4.72%). And was up $11.35 on the week (+13.87%).

OPEC+ agreed to cut oil output by 2 million barrels a day. This would be the biggest production cut since the peak of the COVID-19 pandemic.

WTI Crude Oil (6 month)

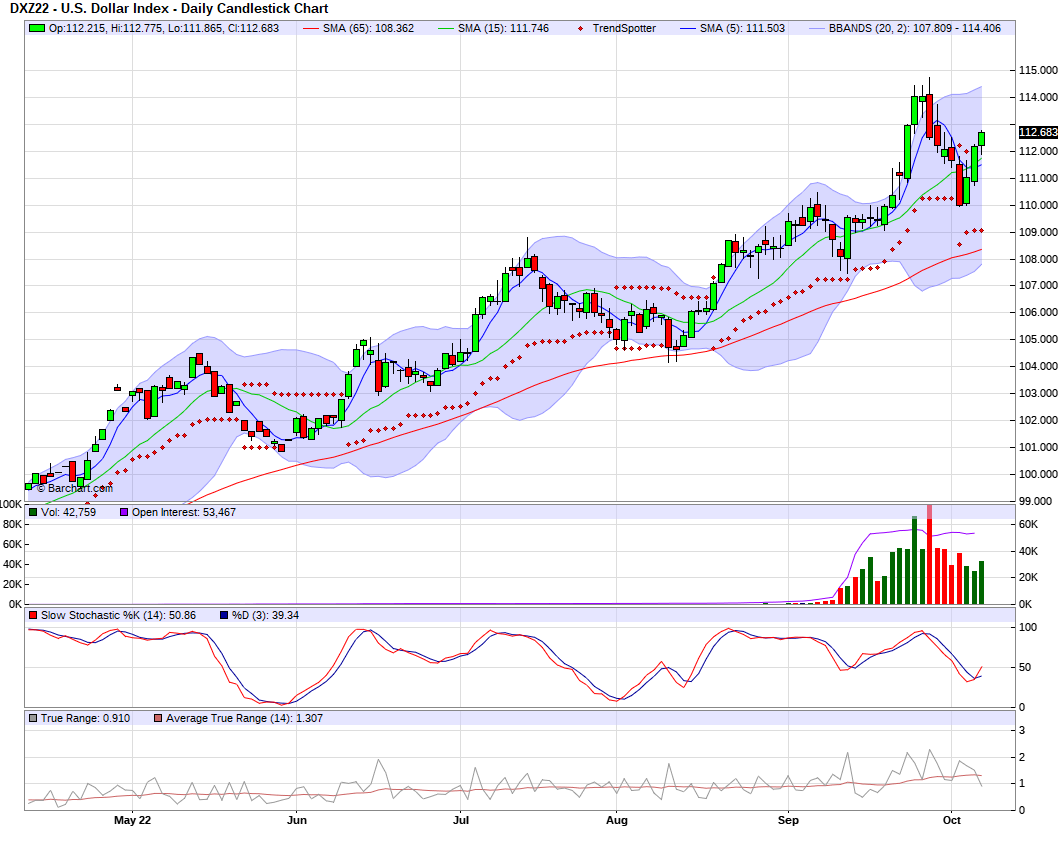

U.S. Dollar

The U.S. dollar started the week off lower. And was down nearly -2% Tuesday. However, the dollar found strength through out the rest of the week and closed the week up .50% higher at 112.747 which is still a ways off our highs we saw September 28th at 114.745

Dollar Index (6 month)

Cattle

Dec live cattle futures ended Friday up +17 1/2 cents, up to $148.05, finishing $1 higher for the week.

Nov feeder cattle ended the week lower -80 cents to $175.625 and was up +$1 on the week.

Dec Live Cattle (6 month)

Nov Feeder Cattle (6 month)

News

The unemployment rate fell from 3.7% to 3.5%, however it was 8,000 more than they were expecting.

It appears the low water levels in the Mississippi river will not be rectified anytime soon. Causing freight rates to raise sharply.

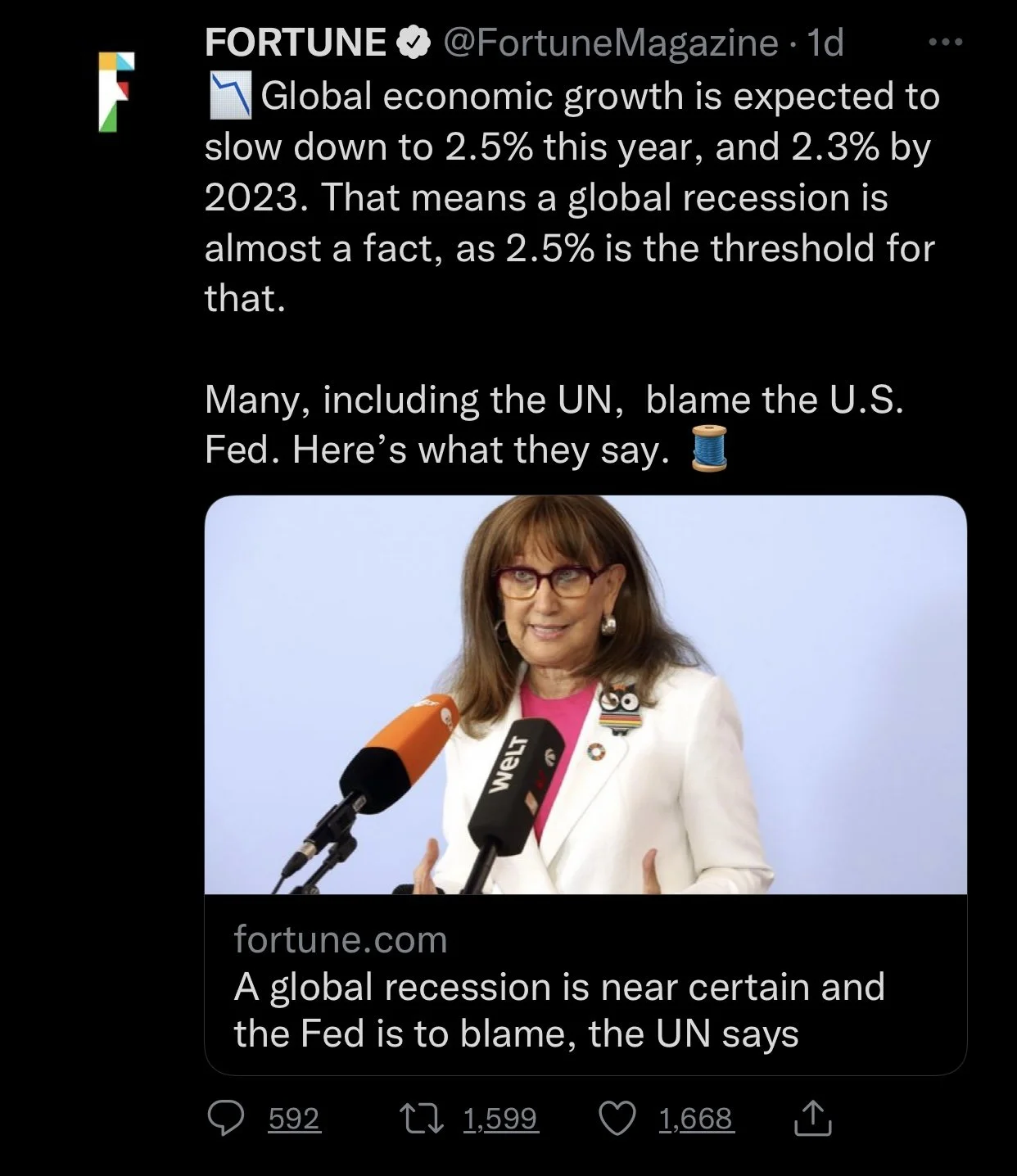

The UN says a global recession is almost certainly coming and the Feds are to blame.

Global economic growth is expecting to slow down to 2.5% this year, and 2.3% by 2023.

EU to cut its corn crop to 55.5 mts, lowest since 2007. France to see worst production in three decades.

Global food prices dropped for the 6th month in a row. With food price index declining -1.1% in September.

We saw record U.S. beef exports in August. With 323.6 million lbs.

In case you missed Friday's audio..

Why do you sell of the combine?

Social Media

Precipitation Forecasts

2-Day

Weather

Source: National Weather Service