USDA TOMORROW

MARKET UPDATE

You can still scroll to read the usual update as well. As the written version is the exact same as the video.

(Main Takeaways at 3:40min)

Prefer to Listen? Audio Version

Futures Prices Close

Overview

Corn & beans lower with some hedge pressure ahead of tomorrow’s USDA report while wheat was higher for the 4th day in a row.

Wheat closed above $6.00 for just the 2nd time since early July.

All the trade is watching tomorrow is the USDA report.

USDA Preview

The trade is expecting slight yield cuts to both corn & soybeans.

Interesting to note that the high guess for corn yield is just a +0.9 increase from last month to 184.5 while the low guess is a -2.0 decrease to 181.6

However, I think the vast majority would not be surprised at all to see yield either unchanged or perhaps slightly higher than last month. As all of the talk is about how fantastic the crop is.

The same can’t be said for soybeans. As most would agree that there is a good chance we saw our highest yield print. With many talking about more disappointing yields than originally expected due to the August and September lack of rain.

I would be in the camp that soybeans saw their highest print already as this could have very well trimmed a little off the top.

For corn, this dryness was too late to make much of an impact.

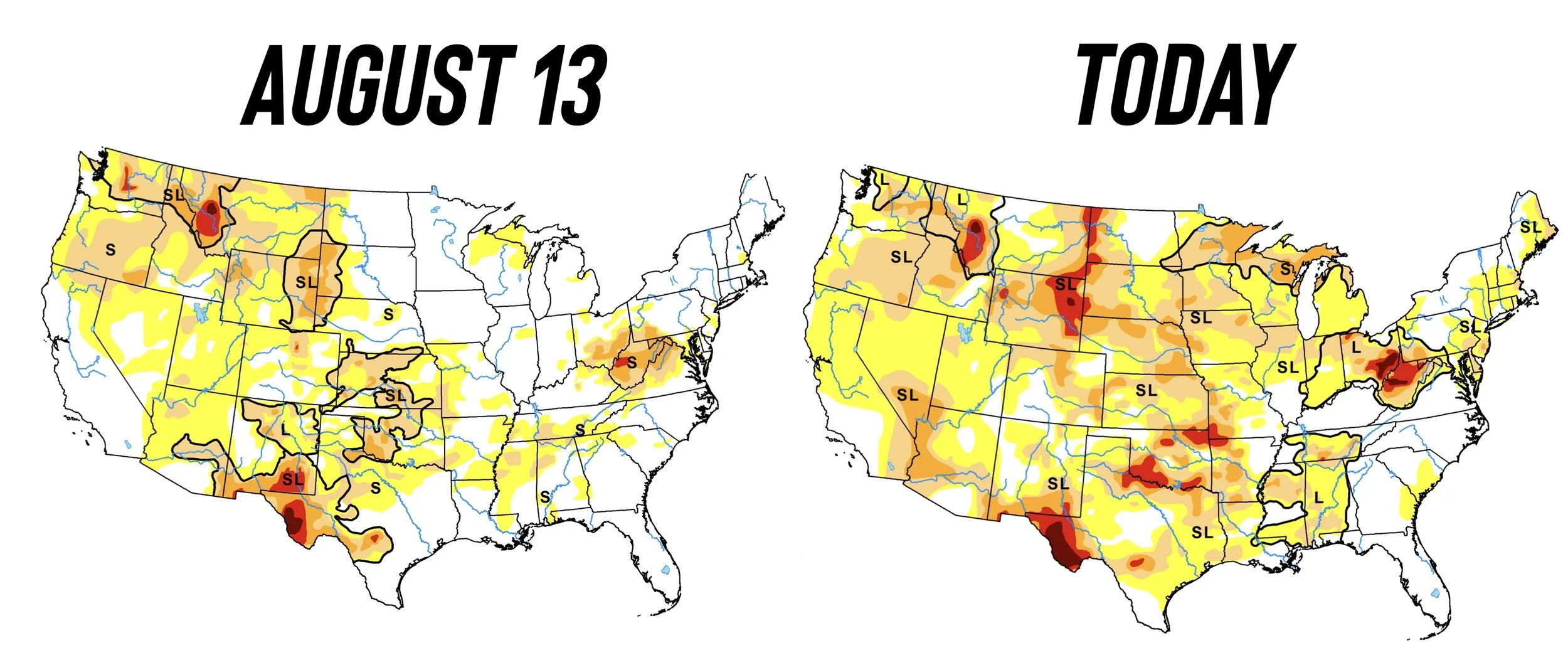

Just look at the drought monitor update.

Drought Change vs Last Week: (Areas in Drought)

Corn: 49% (+22%)

Beans: 43% (+17%)

Spring Wheat: 29% (+7%)

Winter Wheat: 47% (+3%)

(Just a thought.. as it is FAR too early, but one has to question what if this continues into next year?)

Taking a look at US carryout, the trade expects corn to drop below 2 billion bushels.

The USDA is going to increase their projection for old crop feed & residual use for corn. (If you remember, last report the USDA confirmed they were too low on last year's feed & residual demand number).

This alone should be enough to drop us below 2 billion.

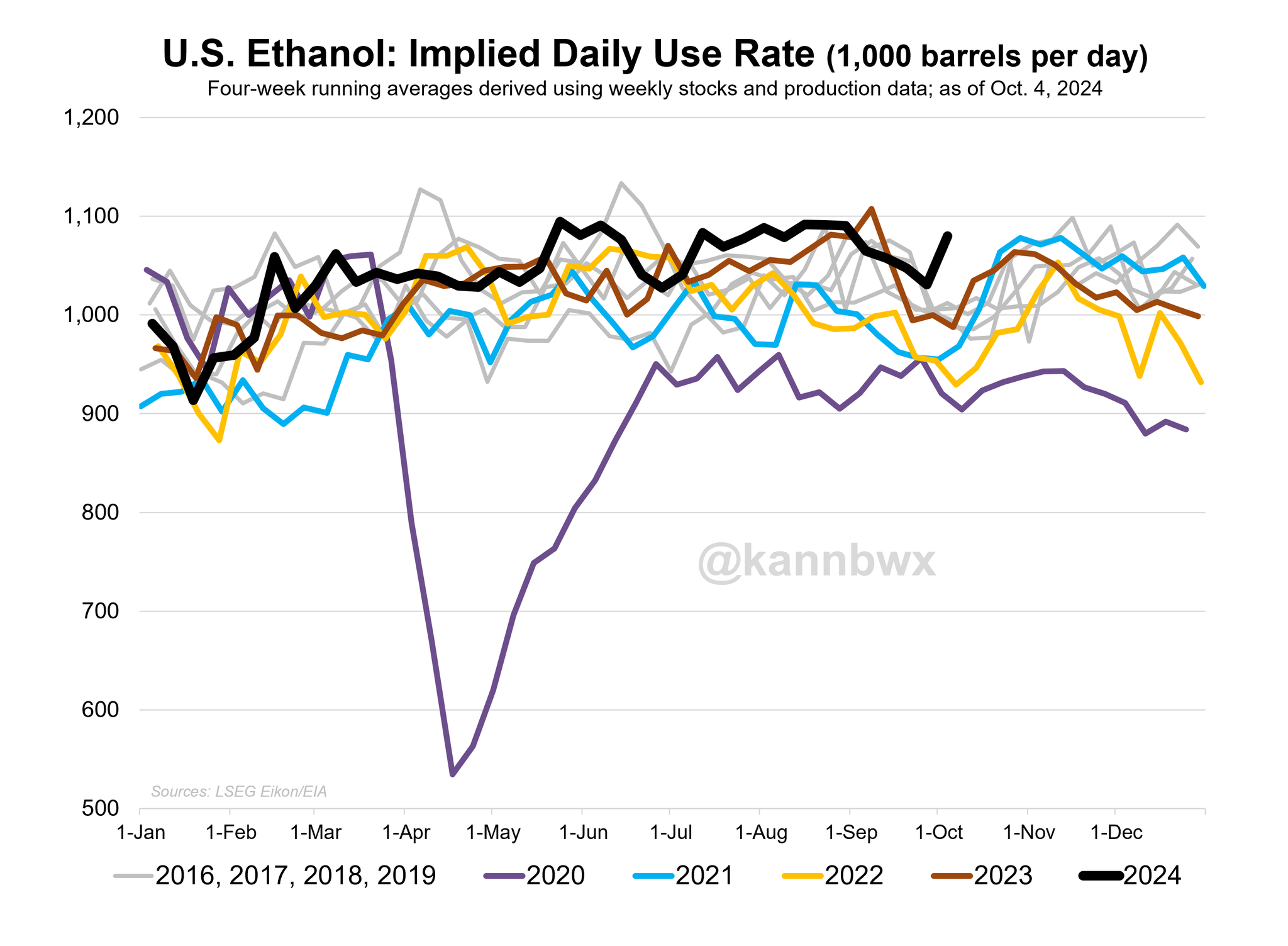

Next I wanted to take a look at ethanol demand.

This is another positive for corn. This won’t make a big difference today, but very well could later in the marketing year.

The current pace of US ethanol demand is ahead of last year while the USDA currently thinks it will be lower than last year.

If we were to continue at this pace, it could add an extra +100 million bushels of corn demand.

Another possible way for us to eat into that carryout.

One could also argue that perhaps the USDA export projections are too low for corn as well.

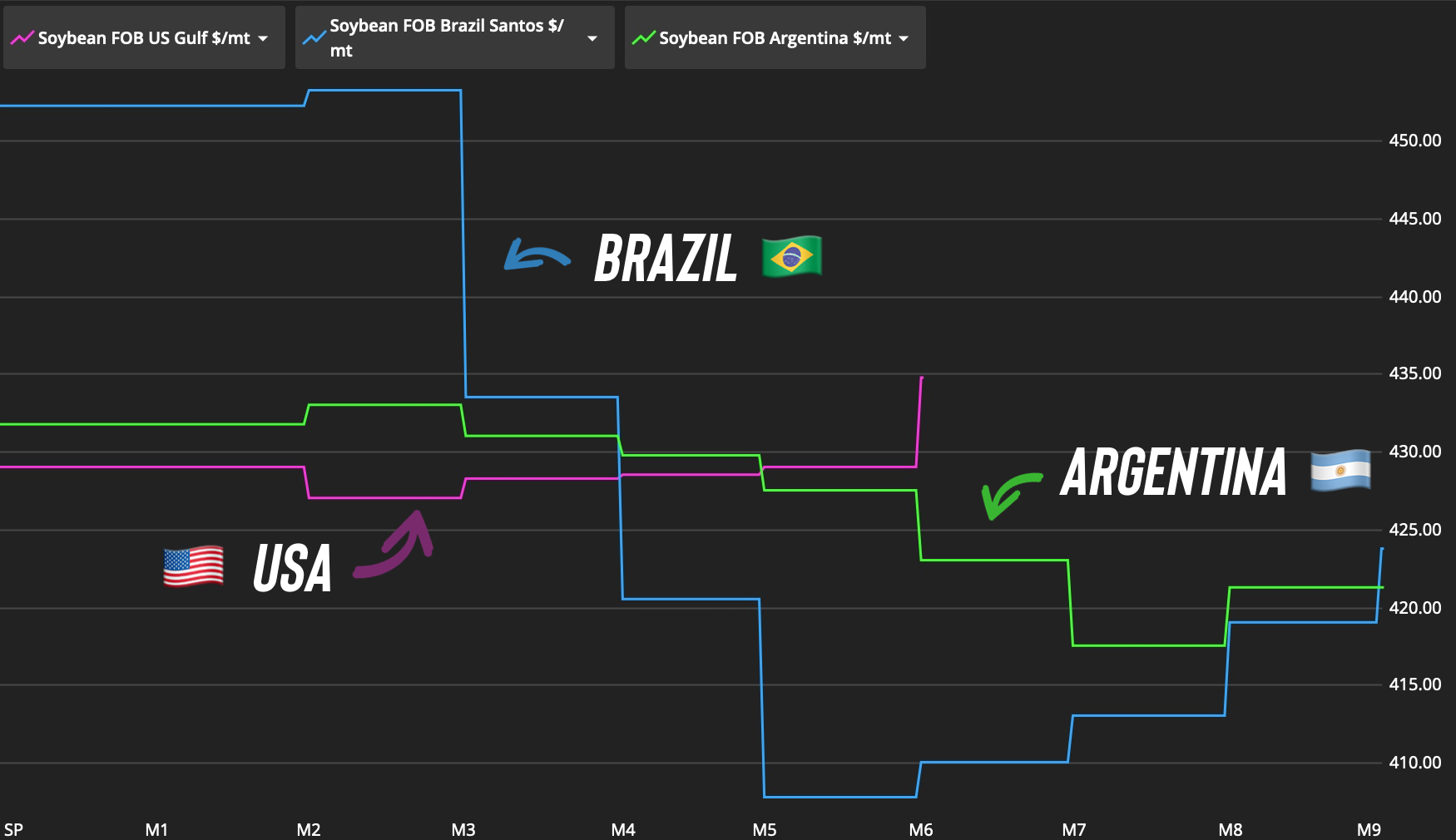

Chart from Karen Braun

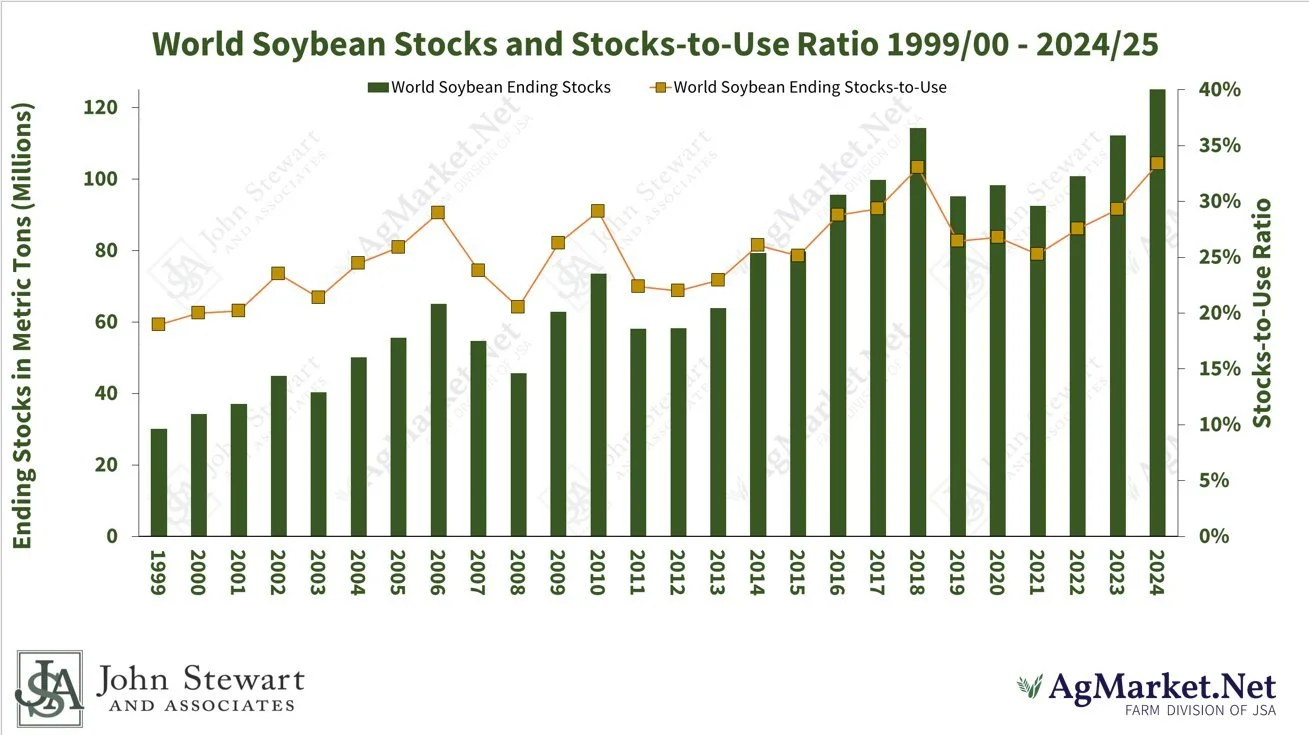

Despite soybeans having the "potential" for lower yields.

The world soybean situation is still very bearish. So keep that in mind.

Our world stocks & stocks to use ratio globally is the highest ever.

Tomorrow’s report will not have a significant impact on the world situation.

We will need a Brazil issue if we want this to change.

Chart from AgMarket.Net

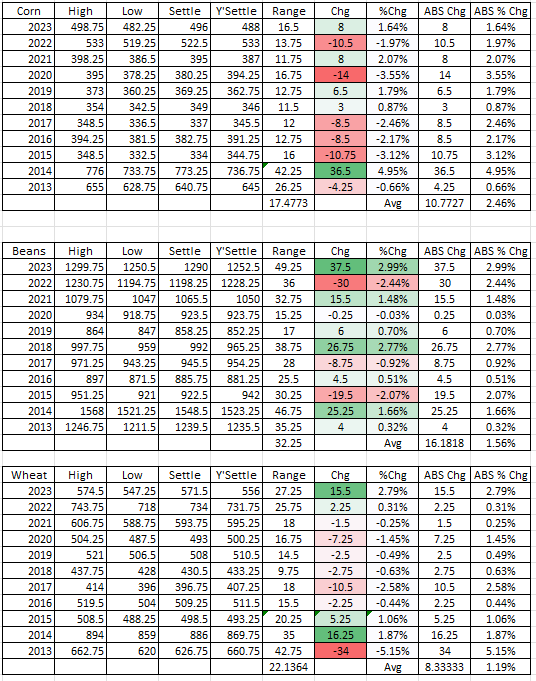

Past Report Performance

This report has been all over the board in the past.

Some year's its a big market mover. Some years it is not.

Here is the past price changes the day of the report:

Chart from WalkSquawk on X

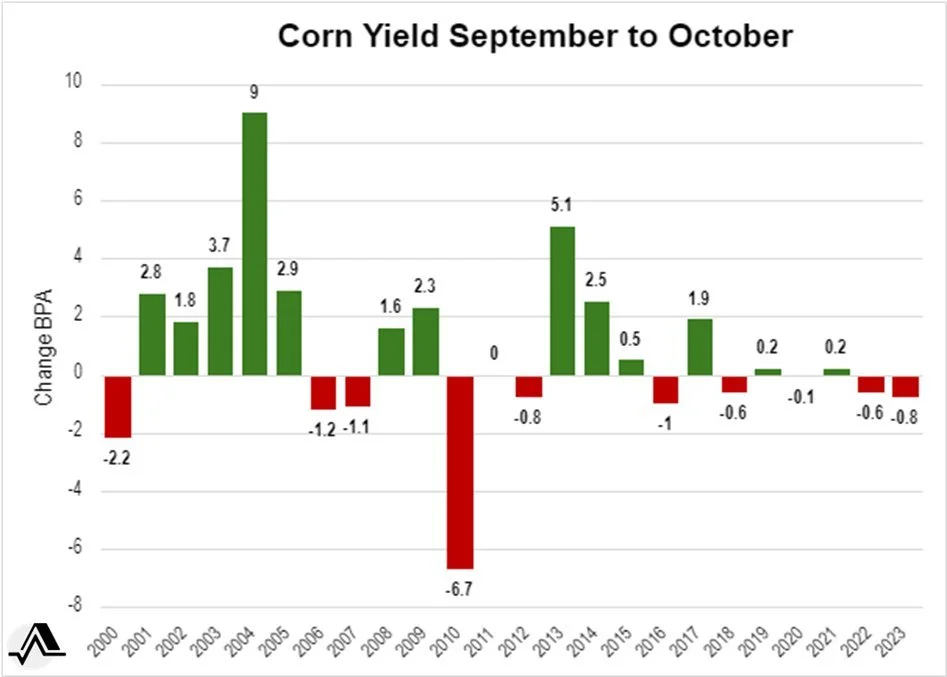

Here is past corn yield changes from Sep to Oct.

We haven’t seen a major change since 2017.

Most expect corn yield to fall within 0.5 a bushel of the estimates tomorrow. That would be between 182.9 to 183.9.

Chart from Allendale

Today's Main Takeaways

Corn

Tomorrow is all about the report.

The biggest potential risk in the entire report is the possibility that corn yield comes in high.

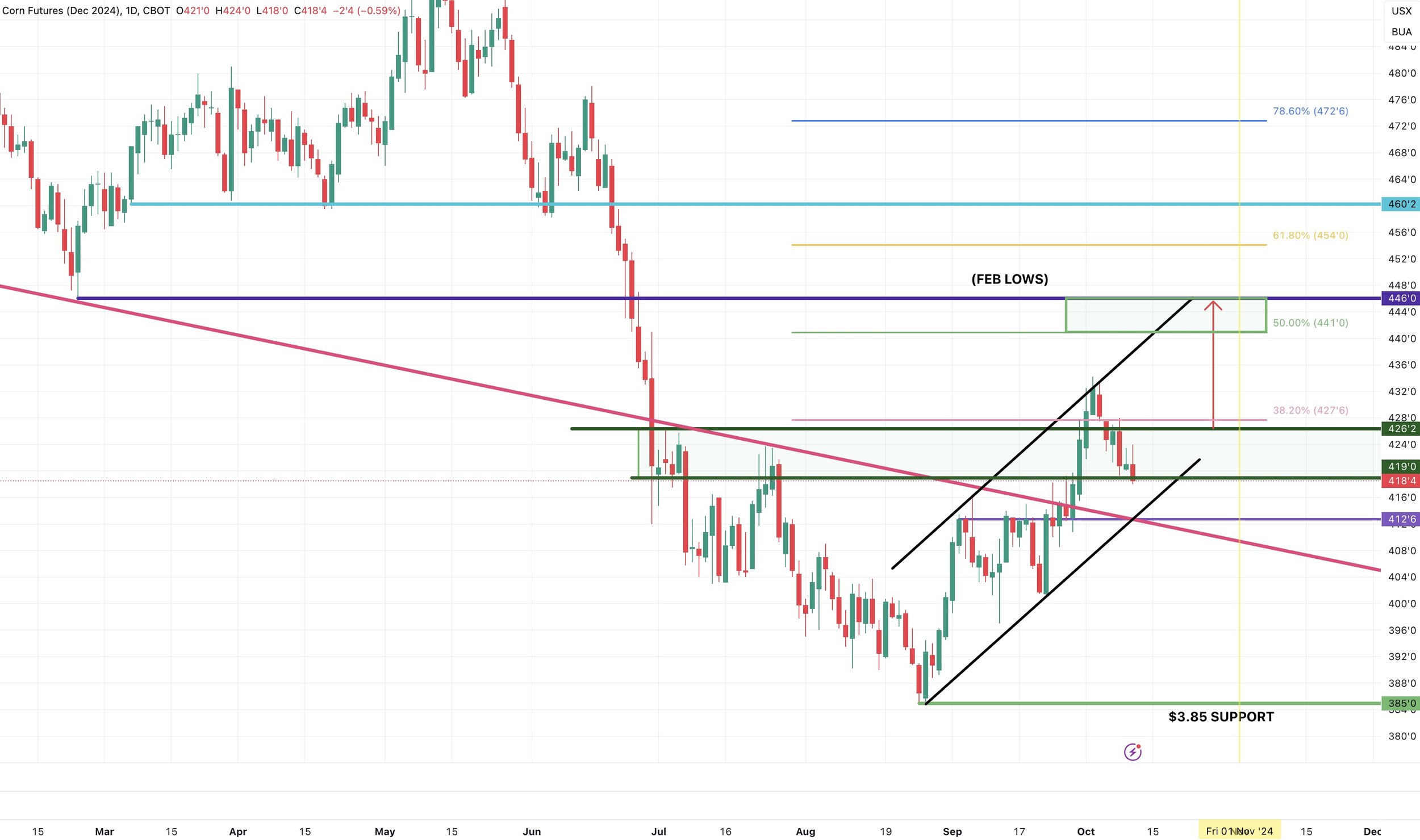

We are still sitting right at some support. So if yield does come in high, we could go to test the bottom end of this channel and that $4.12 area. I would really like to see that level hold.

If yield comes in right at estimates, or smaller, then I like our chances of climbing a little higher.

The corn outlook is far different than the bean outlook. (more bullish)

There are several ways corn could eat into that carryout.

Carryout is already expected to come in below 2 billion tomorrow.

Then we have been seeing great demand. Demand has continued to impressed. While many were talking about how bad demand was a few months ago, I had been stating these prices would create demand.

So we have demand impressing. Our exports continue to impress. We have solid ethanol demand. We are very competitive on the global export market.

Corn yield could very well be up +7 bpa vs last year, yet our carryout could be lower than last year.

Last year our yield was 177.3 vs the 183.4 estimate tomorrow. Last year our carryout was 1.81 billion vs the 1.94 estimate tomorrow. This is possible due to demand.

Then looking to next year, acres could very well be down. High fertilizer prices and costs of production especially at lower corn prices isn’t going to incentivize extra acres. Then we are going to be adding all of this built up demand on top.

To me it just feels like corn is finally finding a story. But it might not happen until harvest is out of the way.

Short term we could still definitely run into some harvest pressure like I have been mentioning since last week. And if that report tomorrow is negative we do still have plenty of downside here short term.

But there is definitely a very valid argument to be made that demand can lead us higher long term.

If you have something to move off the combine, I highly suggest keeping a floor with puts. We alerted a protection signal back when we broke $4.23 for the first time. Now is still a great time to add protection if you have to move something. Especially before a report that could possibly show higher yields.

*Last week we advised a protection signal. (CLICK HERE TO VIEW IT)

Soybeans

Soybeans still sitting at this support zone from $10.18 to $10.00

In my opinion, $10.00 is a must hold. (Chart below)*

If we break below, we have very little support beneath us.

Most seem like if they had to bet on an outcome tomorrow, it would be soybean yield coming in smaller. So we do have that going for us.

But despite this, there is still some tailwinds beans face. Particularly on the global side.

Our global stocks to use ratio is at an all time high. Brazil is getting rain now, so the chance for a delayed planting story are gone.

The number #1 reason for this rally was not the Brazil drought. It was the China stimulus story.

The trade is not concerned with Brazil. We have already removed the little bit of the weather premium we had. Which means that these rains are not going to pressure us here.

However, if Brazil raises a bumper crop there is a LOT of downside risk in beans.

It is just hard to find a majorly bullish story in beans unless one of the following happens:

China continues to pump money into their economy

China decides to buy a lot more beans

Brazil has a crop scare

Any of these can happen. If they do, they will be game changers. But they are all wild cards & impossible to guess. Without any of those happening, there is still major risk to the downside here in beans.

Unlike corn, there isn’t a ton of different ways to paint the balance sheets more friendly.

One positive beans do have is that they are very competitive on the global export market. Beans off the US Gulf are the cheapest in the world until Brazil's crop comes online early next year.

Then of course there is a decent chance yield could drop. Which would be beneficial for prices, but not enough to create a massive bull run.

The China or Brazil stories on the other hand all have the potential to send beans another $1.00 higher... or $1.00 lower if none of them happen.

Risk Management:

We alerted a sell signal on Friday Sep 27th's highs. (CLICK HERE TO VIEW)

Since then, we have given back exactly 50% of the rally.

If you followed the signal and grabbed puts, it is never a horrible idea to lock in that profit. But many of you may want to wait until you make a physical sale to lock in that profit.

Traditionally, you want to wait until you make a sale to sell the puts. But an aggressive approach would be to lock in that profit now, then wait for a bounce to make that cash sale. The only risk is if that bounce doesn’t come.

Now if you sold calls as an example for 15-20 cents, and you can now buy them back for a few cents. It does make the most sense to re-buy those so you don’t have that risk out there. Especially in a scenario where you have captured 90% of the maximum you can make on a sold call.

If you are someone who did not do anything, and still does not have protection. Then you should get some ahead of the USDA report. ESPECIALLY if you have to move something off the combine.

If you have questions, give us a call or text (605)295-3100. As you are all in different situations.

Wheat

Wheat isn’t the big thing traders are watching tomorrow, as corn & soybean yield adjustments are going to steal the show.

But the wheat situation does still look pretty friendly as of today.

One of the biggest things that had been keeping a lid on wheat prices since the initial war was cheap Russian prices. But their prices have started to creep higher.

If global wheat prices have indeed found a bottom, then it is a huge supportive factor for us.

The Russia drought is still the biggest thing to watch in the coming months. For now it is not a huge factor, but it could be.

Russia is the world's #1 exporter & producer of wheat. Their exports are already down -10% from last year.

World wheat stocks have continued to fall year over year.

Just feels like wheat also potentially has the possibility to climb higher.

Risk Management:

We recently had a few wheat sell & protection signals.

One on Sep 13th at $5.99 and the other on Oct 2nd when we hit my first target of $6.12

If you have not took some risk off the table yet, now is still a good time to do so.

If you have taken risk off the table already, I like being patient from here.

Next target is still $6.40 (our 50% retracement to May highs)

Want to Talk?

Our phones are open 24/7 for you guys if you ever need anything or want to discuss your operation.

Hedge Account

Interested in a hedge account? Use the link below to set up an account or shoot Jeremey a call at (605)295-3100.

Check Out Past Updates

10/9/24

MARKETING STYLES, USDA RISK, & FEED NEEDS

10/8/24

BEANS FALL APART

10/7/24

FLOORS, RISKS, & POTENTIAL UPSIDE

10/4/24

HEDGE PRESSURE

10/3/24

GRAINS TAKE A STEP BACK

10/2/24

CORN & WHEAT CONTINUE RUN

10/1/24

CORN & WHEAT POST MULTI-MONTH HIGHS

9/30/24

BULLISH USDA FOR CORN: RECOMMENDATION

9/27/24

UP-TOBER? SELL SIGNAL, TARGETS, & FACTORS

9/27/24

BEAN SELL SIGNAL

9/26/24

NEW HIGHS BUT CONCERNING CLOSE

9/25/24

HIGHEST CLOSES SINCE JULY. UPSIDE & SALES CONSIDERATION

9/24/24

GREAT START TO THE DAY, AWFUL FINISH

9/23/24

MASSIVE DAY FOR THE GRAINS

9/22/24

EARLY YIELD TALK, DROUGHT, BRAZIL, SEASONAL LOWS & MORE

9/19/24

GRAINS SEE TECHNICAL SELLING

9/18/24

FED DROPS RATES, BRAZIL STORY, 2025 SALES?

9/17/24

TARGETS & WHAT TO DO IF YOU BOUGHT PROTECTION

9/16/24

WAS TODAY HEALTHY CORRECTION BEFORE GRAIN RALLY RESUMES?

9/13/24

CORN & WHEAT BREAK OUT: EVERYTHING YOU NEED TO KNOW

9/12/24

USDA RAISES YIELD BUT REPORT WASN’T ALL THAT BEARISH

9/11/24

USDA TOMORROW. MAKE OR BREAK SPOT ON CHARTS

9/10/24

USDA THURSDAY

9/9/24