GRAINS STRUGGLE TO FIND MOMENTUM

Overview

Grains unable to move higher today after initially trading higher. As all grains see minor losses today. With chance for Argentina rain and preparation for the USDA report put a lid on the grains today.

With fund rebalancing this week, they are talking about the funds selling corn, wheat, and beans. Which could have been the case with the minor losses across the board today as we did open higher but we unable to hold those gains.

The warmer temps in the U.S. adding some pressure to the corn and wheat markets.

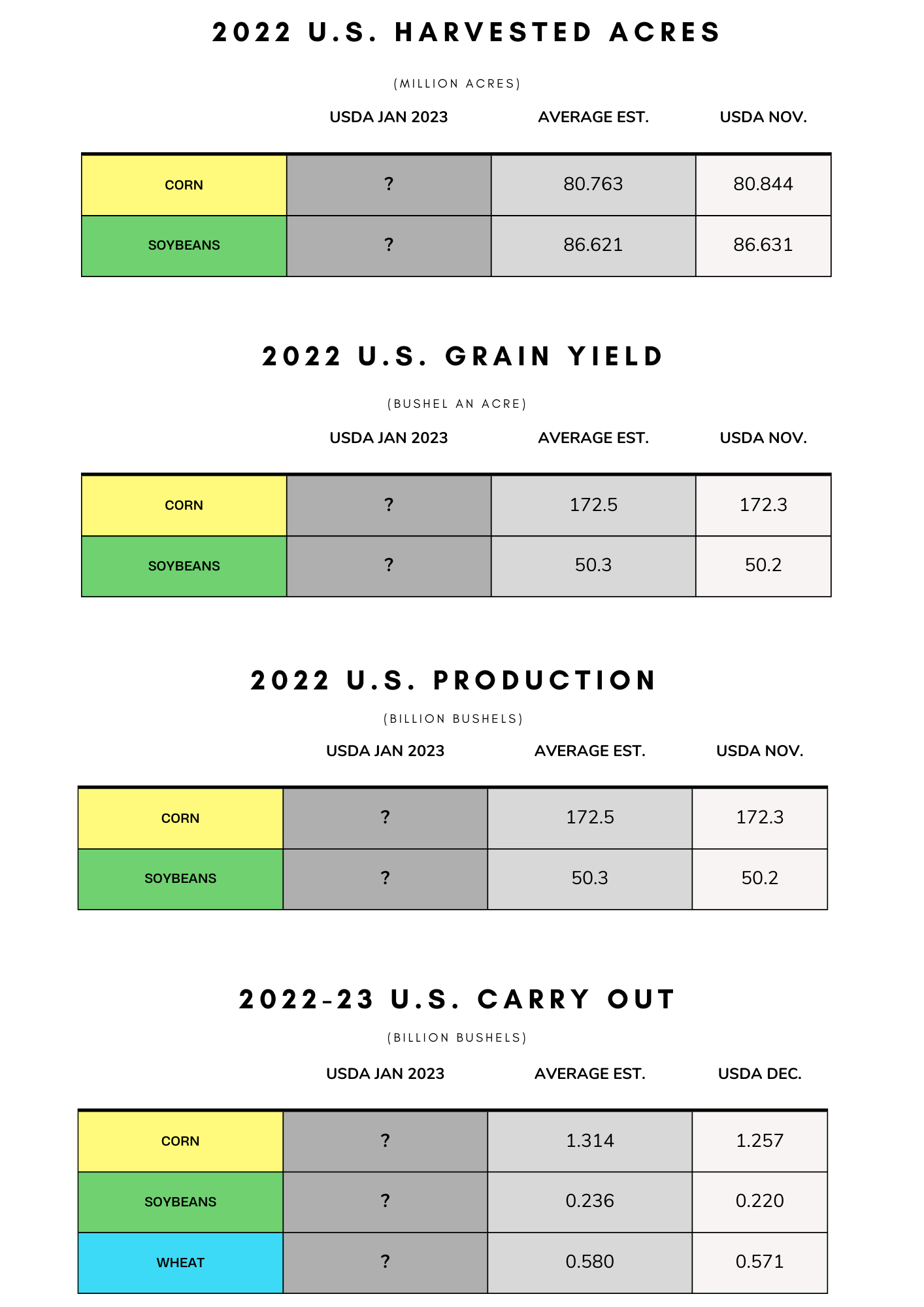

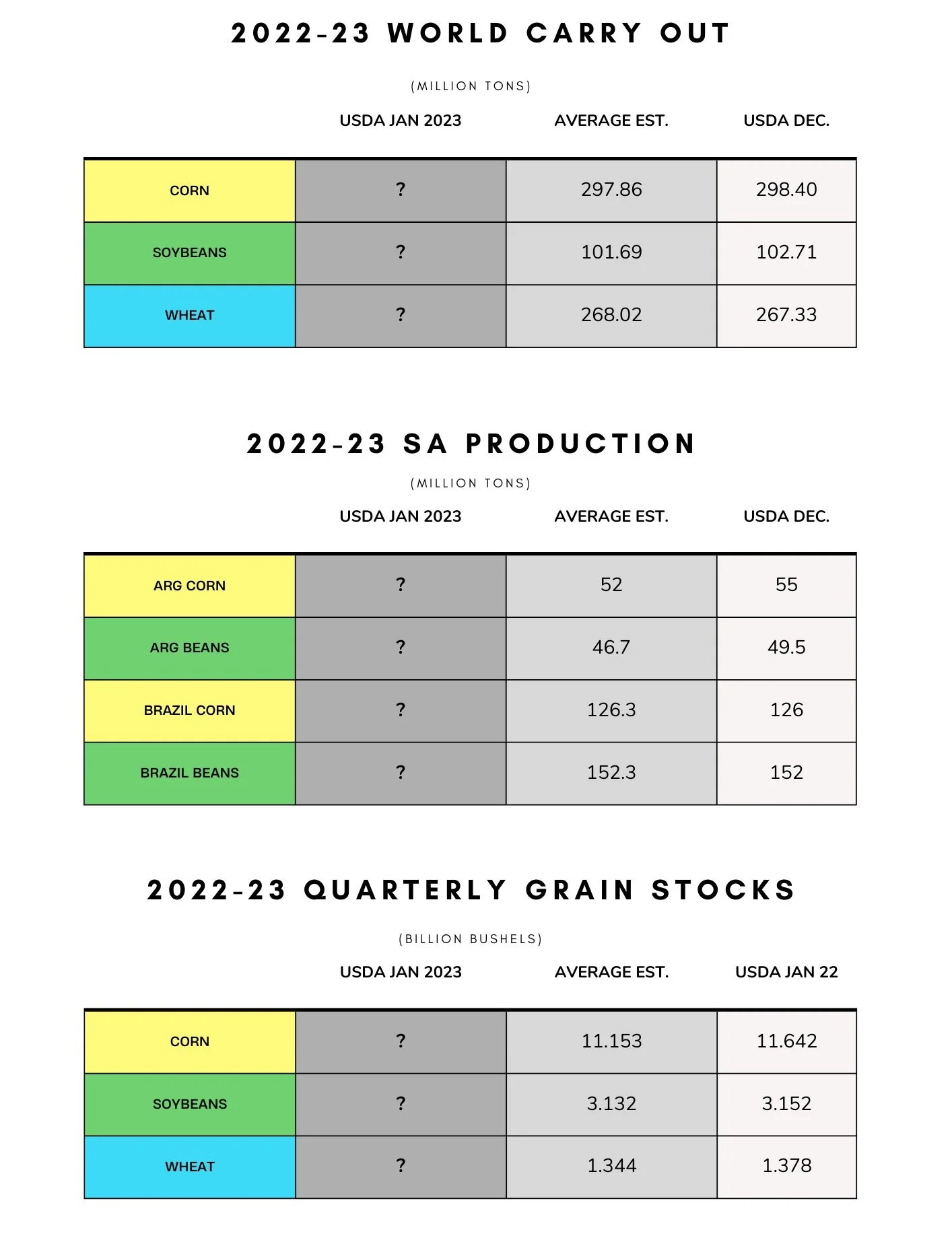

In the USDA report, they are looking for slightly higher carry outs, slightly lower exports, and higher production across the board.

We can expect some volatility going into the end of the week as the trade tries to position itself ahead of the USDA report and of course we will some big moves after as well.

If you missed it, read yesterday's full version of our Weekly Grain Newsletter Here

Today's Main Takeaways

Corn

Corn failed to move higher to start the week, trading in a tight range and ultimately closing down just a penny.

Last week we saw corn futures lose almost -25 cents on the sell off across the grains. But corn did hold up better than that of beans and wheat. Since around October anything $6.80 or higher has remained a pretty stiff resistance.

There are a few factors that will continue to influence the corn market, but the USDA report this Thursday is the biggest one. It seems like most think we will see the USDA again trim demand, and possibly raise U.S. production estimates.

Going into the the report, we might see the bullish funds take a step back here. After the report, the main focus will again shift to South American weather and other macro headlines.

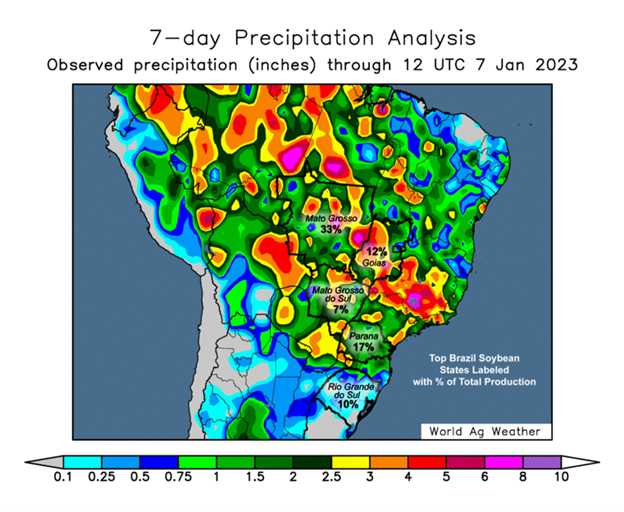

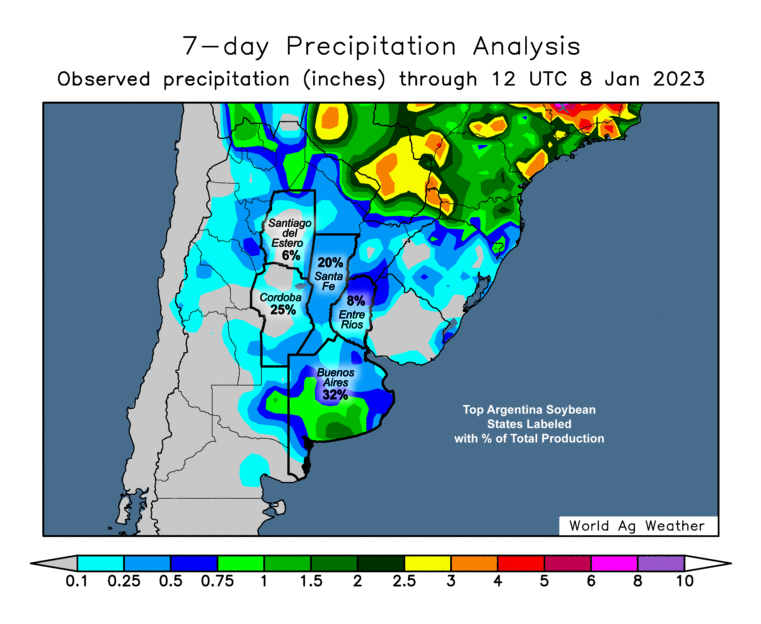

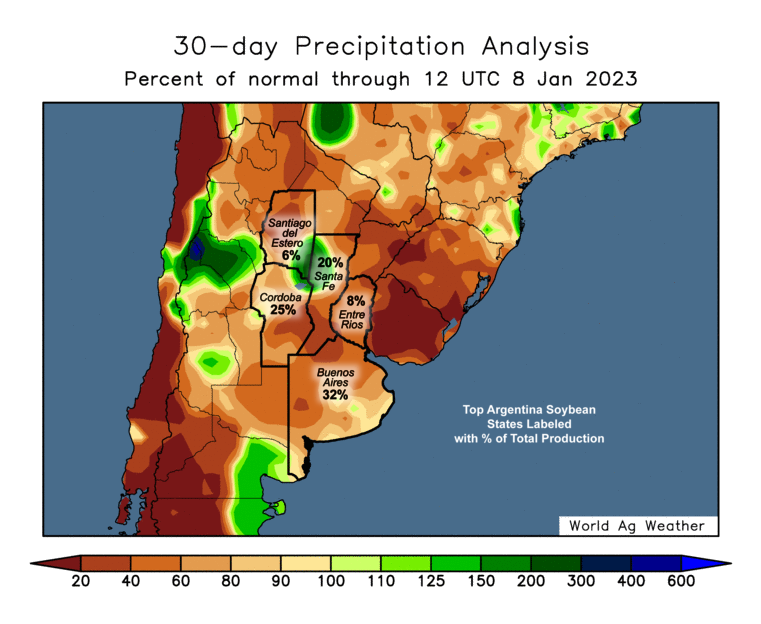

Taking a look at South American weather, Argentia remains the main headline everyone has been focusing on. As they have remained dry and face a ton of complications. We also have an entire season ahead for South Americas corn crop, which is Brazils second crop.

Outside of the USDA report and South America, the other two main things that will likely influence the corn market is the war in Ukraine and covid in China headlines. The war has been a problem for so long that sometimes the trade ignores when we see escalations. China is facing plenty of problems with covid and their economy, as there is still talks about a possible recession. Will there economy improve or fall further, and how does this impact demand. Those are the two questions surrounding China.

Corn March-23

Soybeans

Soybeans ended the session today down -4 cents at $14.88 1/2 after trading as high as almost $15.02 early in the session. Soybeans struggled to move higher and the dry Argentina forecasts just weren’t enough to hold prices higher as we ran into some selling.

Soybeans lost over -30 cents in the sell off last week, so bulls will be trying ti regain some of those losses. Despite the sell off, beans are still only 10 cents under $15.

Taking a look at the USDA report. We have a somewhat similar story to corn. Argentina will probably draw the most attention, but in the U.S. most are thinking we see the balance sheet perhaps a little larger.

There is still a ton of debating going on regarding the expected record crop in Brazil, as well as a limited supply of bean meal. As some are thinking the reduced meal supply from Argentina might just be enough to support prices and combat against Brazil’s massive crop. Soymeal just made a new contract high and there is some talks we might see meal go back to test all time highs which were made back in 2012.

Argentina has the been the main story for some time in the bean market. It looks like Argentina might get some widespread rains later this week. If they do get a bunch, we could beans under some pressure. So the question going forward this week is how much rain will they actually get, and how much will this actually improve their yield. For the USDA report, its pretty clear we will likely see cuts made to Argentina production in both corn and beans.

Outside of South American weather, which will continue to be the biggest factor in dictating the direction for beans, we have China. As Chinese demand and covid will be the other headline traders are watching.

Soybeans March-23

Wheat

Wheat followed the rest of the markets slightly lower today with lack of bullish news. Chicago wheat traded almost as high as $7.60 before ultimately closing 17 cents or so off our highs at $7.41 1/2.

Wheat futures lost over -40 cents last week as all grains took a dip to start the new year. Bringing all classes of wheat near the bottom of their range trade as we failed to break a few key resistance levels. A well respected advisor Roach Ag gave out buy signals for wheat today.

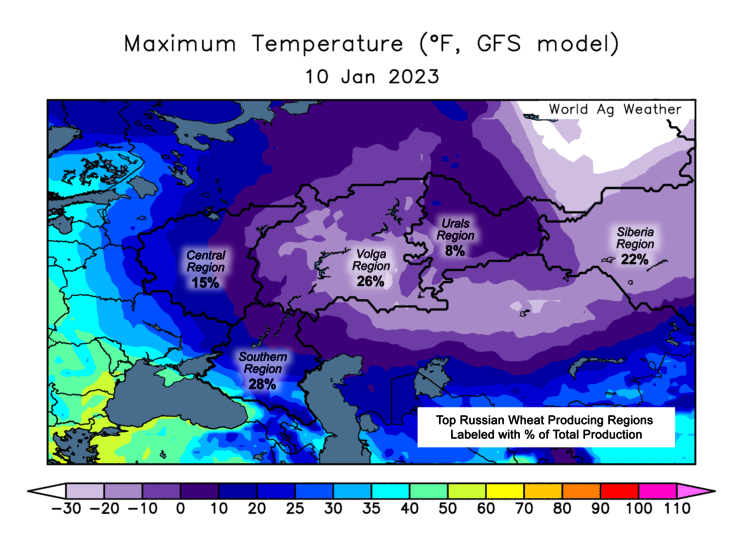

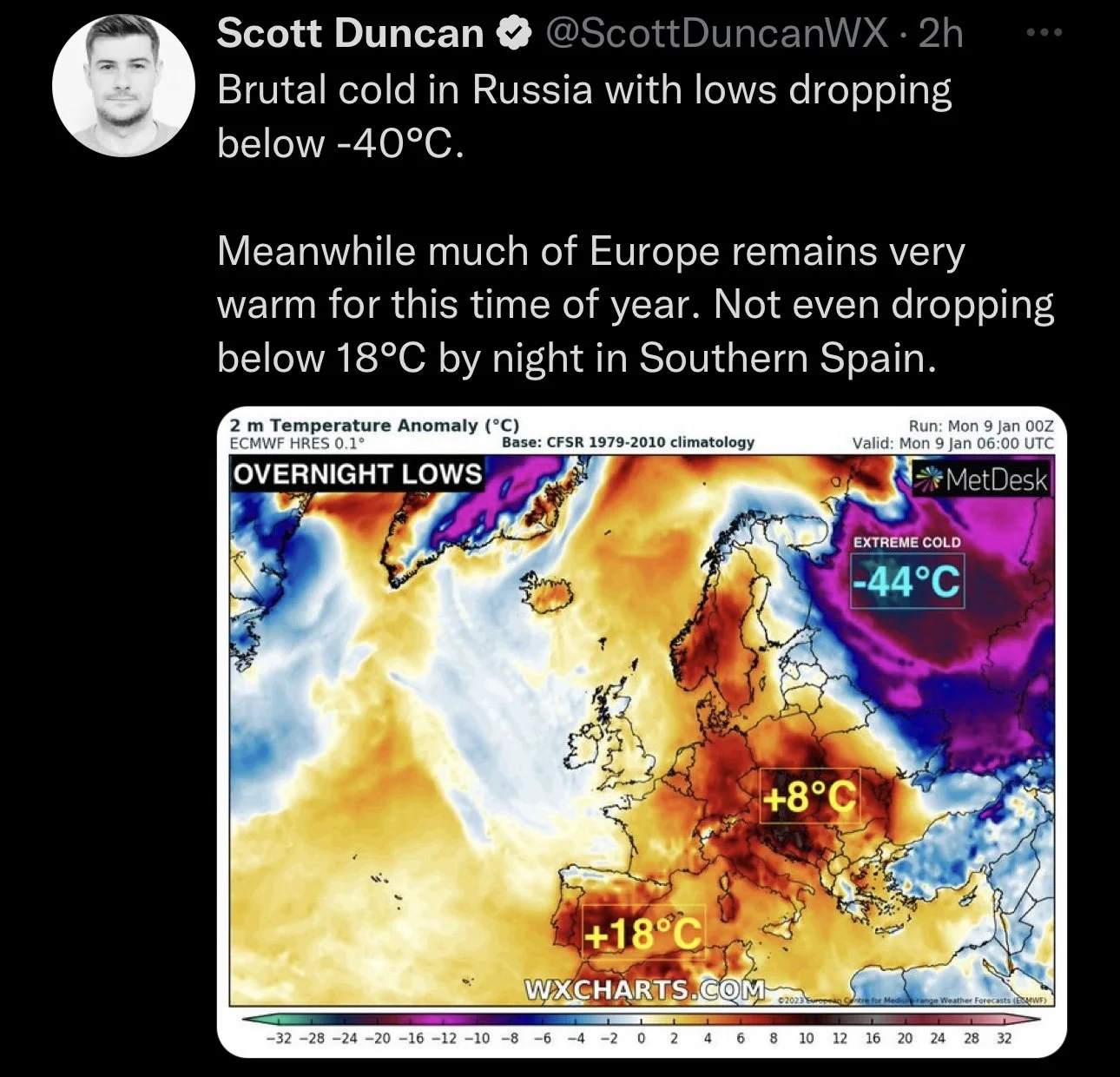

Wheat has been pressured by the rather large crops out of Australia and Russia. As Australia is expected to have a record crop of 42 million metric tons, and we have all heard of Russia's massive crop. But on the other hand, there is still a chance we see Russia see some winter kill some time this week with the brutal temps and lack of snow cover. We also have Argentina's crop getting smaller and the U.S. winter wheat is still in poor shape.

Funds continue to be short Chicago wheat. As they have continued to add onto their historically short position in Chicago wheat since July.

U.S. winter wheat has seen some pretty good moisture, but the one area of concern is still western Kansas. But will all the rains coming in from the west coast there is a chance we do see western Kansas get some rain.

Thursday's report will be a big one for wheat, as if you remember we didn't get a ton of new data in the last report as it is typically saved for the January one. We will receive the yearend report, quarterly grain stocks, and winter wheat seedings. All of which will provide a ton of info. So we will have a ton of different information being released all at the same time. We will have to see which one steals the show. One thing to note is that they are looking for a pretty big increase in U.S. wheat acres.

If we get a ton of bad news in the report that sends wheat falling, I would look at that as a great buying opportunity for the long run. But nonetheless, the wheat market will continue to play the weather and war game going forward for the time being.

Below is a chart from Wright on the Markets with the tag line "Do not be in a hurry to price 2023 wheat".

Chicago March-23

KC March-23

MPLS March-23

USDA Report Estimates

Analysts are expecting a snoozer for 2022 U.S. corn and soybeans in the USDA report Thursday. As they are expecting historically small changes in harvested acres, yield, and production. But with these projected small changes, leaves the window open for some curveballs.

As for ending stocks, corn is expected to see the largest rise due to smaller demand. Their current estimate is still lower than that of 2021-22.

Most are expecting growth in Brazil's corn and bean crop, but a very big decline is expected for Argentina crops.

Soybean Meal from Wright on the Markets

This is a great write-up from Wright on the Markets talking about soybean meal and crush capacity. You can visit their website here

They said,

There are about 60 soybean crushing plants in the USA with a crush capacity of about 2.2 billion bushels per year. The end of the 2022 numbers show there are 23 crush plants being built or expanded. Crush capacity was expanded by about 110 million bushels in 2022 and that is just the beginning. By 2026, US crush capacity is projected to be 3 billion bushels. The USDA projects the soybean crush this marketing year will be 2.245 billion bushels, up from 2.2 billion last year. Six months ago, the outlook was that soybean production would need to increase 640 million bushels to meet the new crush demand in 2026. Current projections are that 760 million bushels will be needed to meet the 2026 soybean crush demand. That will take 14 million more acres of soybeans. Goodbye to a lot of corn, sorghum, wheat and cotton acres. Imagine the bidding war for acres in the coming years!

The 2023 soybean crush construction is projected to expand crush capacity by 300 million bushels. More than a year ago, analysts predicted that within 4 to 5 years, the USA would not export a single bushel of soybeans. All US beans would be crushed for the oil to be used for Sustainable Aviation Fuel (SAF) and the US would replace Argentina as the world's leading soybean meal exporter. If you look at our weekly export sales analysis on yesterday's mailing, you will see marketing year-to-date sales of soyoil is 37,100 mts; a year ago this date, the soy oil sales were 440,700 mt.

We have been talking about the recent very strong soybean meal prices. Consider this: What do you think will happen to soybean meal prices as the crush capacity rapidly expands?

All of this is due to the current “green energy” program resulting in more demand for biodiesel to some extent, but primarily for Sustainable Aviation Fuel (SAF). To learn more about SAF, go to: https://www.wrightonthemarket.com/post/saf-will-change-your-life

U.S. Basis/Cash from TFM

You can visit TFM's website here

Basis bids for soybeans shipped by barge to the U.S. Gulf Coast for export were flat to lower on Friday as freight costs eased for a second straight day and river shipping conditions improved, traders said.

Rising water levels on the Mississippi River and its tributaries allowed shippers to haul more grain per barge. River navigation snarls earlier in the week due to foggy weather were also easing, shippers said.

Freight rates for January barges fell by 50 to 75 points of tariff for a second straight day on Friday as demand slumped for empty vessels for near-term shipment, barge brokers said. BG/US

Spot export premiums were flat despite easing CIF basis values. The values were underpinned by light demand for near-term U.S. shipments before newly harvested Brazilian corn and soybeans flood the market starting in February, traders said.

Chinese importers have made some price inquiries for February soybean shipments from the U.S. Gulf Coast, a trader said.

CIF basis bids for soybean barges loaded in January fell 7 cents to 110 cents over March. February barges were bid a penny lower at 104 cents over futures.

FOB offers for soybeans loaded at the U.S. Gulf in January held at 150 cents over March.

CIF corn barges loaded in January and in February were bid 2 cents lower at 90 cents over March.

Export premiums for January corn loadings were unchanged at 125 cents over March futures.

Spot basis bids for corn fell at rail terminals across the eastern corn belt on Friday, grain brokers said.

Corn basis eased in Evansville, Indiana and Columbus, Ohio.

Bids for soybeans were steady across the U.S. Midwest.

Spot basis bids for soybeans were mostly softer on Friday at river terminals and processors across the U.S. Midwest.

Bids for soybeans fell at a Decatur, Indiana processor and a Seneca, Illinois river terminal.

Corn bids were even on Friday.

Spot basis bids for hard red winter (HRW) wheat firmed on Thursday for wheat shipped to the U.S. Gulf by rail.

Bids for wheat across the Southern U.S. Plains were steady, dealers said.

Protein premiums for hard red winter wheat delivered by rail to or through Kansas City fell by 10 cents a bushel on Friday for wheat with protein content of 11.8% and dropped 15 cents for 12% to 14% wheat.

Spot basis offers for soymeal firmed at rail terminals across the eastern U.S. Midwest on Friday, as well as for barges loaded upriver of the U.S. Gulf and at the Gulf, brokers said.

Availability of rail cars in the Midwest remains tight, one Kansas City rail dealer noted.

Offers at truck terminals were steady.

Predictions from Zero Hedge

This was included in yesterday’s weekly newsletter but I thought I would again share a few insights and predictions they made. You can read the full article from Zero Hedge here as these are just a few they made.

1) Inflation will return with a vengeance

What we’ve experienced so far came from the big commodity pump-and-dump post-COVID. Commodities went through a massive run as more money chased broken supply chains in 2020-21. Then in 2022 the inevitable bust happened, but left us with commodity prices across the board at levels which used to be resistance on the long-term price charts which has now become support.

The next round of commodity-based cost-push inflation will mix dangerously with the growing realization that we can’t avoid things breaking. There will be no ‘soft landing.’ The hard landing may not happen in 2023, but the set up for it will certainly take place.

Cost-push will mix with Loss of Institutional Confidence to light the fire of real inflation versus tangible assets in a way we haven’t seen since the late-1970’s. We should see a return to increasing YoY CPI levels beginning in Q2 after the baseline effects are past and China’s reopening keeps a bid under commodities.

January will not set the tone for commodities in 2023, but more likely be a ‘false move’ overcorrecting against the primary trend, which is clearly higher.

4) The War in Ukraine Will Continue Dangerously

The West is suffering under many illusions about what’s going on in Russia and, by extension, its war in Ukraine. The UK/US neocons believe, like the EU, that history is already written about Russia’s future –balkanization and collapse.

All pressure that the West places on Russia only exacerbates their demographic time bomb. China’s as well. And in that sense this is the race they are running. Can they grind up enough Russians to ensure that even if Russia wins the war in Ukraine the West wins because the long-sought breakup of the USSR/Tsarist Empire will be achieved.

For this reason neither the UK/US Neocons nor Davos believe having a reverse gear vis a vis Russia is the right play. This is their strategic vision, regardless of the costs to the West itself.

For Russia there is no other play for them but to continue increasing the costs on the West. The longer the war goes on the deeper divisions within the EU get. Those divisions then drive even more animosity within the Eurocracy towards the Brits and the Yanks, who some feel are taking advantage of the situation.

When as ardent an Eurocrat as Guy Ver Hofstadt is now frothing at the mouth about the costs of sanctions, you know the Mafiosi in Brussels are getting nervous. They are beginning to crack under the strain of this war of financial and political attrition Russia is so good at playing against its European partners.

Even though I’ve argued strenuously that the EU leadership walked into Ukraine with its eyes open, the 2nd tier of the Eurocracy did not. And those are the ones having cold feet now and who the Russians are hoping will drive a pivot from Davos off Ukraine.

At the same time, expect Putin to keep opening up new fronts for the US/UK to deal with, see my next point.

The UK/US Neocons’ only play, then, on the battlefield then is further escalation to the brink of a nuclear exchange, which these insane people think they can win.

The other option is assassinating Putin in the hopes that Russia goes mad, nukes someone and that justifies the unthinkable.

Either way we’re inching way too close to midnight for my tastes.

6) De-Dollarization Will Accelerate / USDX Will Rise

Along with the collapse of the euro, the US dollar will lose more ground in the global payment system for international commodities and trade.

These two dynamics will create a very weird moment where the USDX — the US Dollar Index — will rise but the US dollar will be under sincere pressure vs. gold, commodities, and other rising emerging/developed market currencies.

The USDX is heavily weighted towards the euro and the British pound but the Chinese yuan is not represented at all. So, from one perspective the US dollar could be in a bull market but from another be in a bear market.

The one thing holding gold back has been its lack of bull market versus the dollar. It’s not a ‘secular’ bull market in gold until it’s rising versus all currencies. Even if the USDX does nothing but hold its ground in 2023 versus the rest of its fiat competition, a rally in gold will still be fed by people the world over ‘losing their religion’ with respect to the dollar.

That said, that fall in faith will likely not outpace the fall in faith of the “Fed Put.” I expect the ‘religion’ of the Fed Put is still stronger than the dollar itself which should put upward pressure on the US dollar overall. Because, let’s not forget that overseas US dollar synthetic short positions, known as US dollar-denominated debt, are still pretty biblical in size, keeping a strong bid under the dollar globally even as its position as a reserve and trade settlement currency erodes.

Because of all of these competing forces — inflation, de-dollarization, war, etc. — the last US dollar bull market for the foreseeable future should be on tap in 2023. For how long? It’s a good question, I can’t answer.

8) Oil will Open 2023 Near the Yearly Low

The fundamentals for oil are truly bullish. China ending Zero-COVID just after the EU put its idiotic price cap on seaborne Russian oil was a strategic move to subvert “Biden’s” wish to refill the now nearly depleted US Strategic Petroleum Reserve at or below $70 per barrel.

He may get that from domestic producers for a while. But Brent ended 2022 at $86 and a little downside momentum may be in place with early US dollar strength, but then fundamentals easily overcome this.

“Biden” will not refill the SPR at $70 per barrel now that China just blew up the entire “deflation through higher rates” narrative. The US economy has held up better to the Fed than expected. Even Q3 GDP wasn’t uniquely terrible. The jobs report and low unemployment rate, while possibly artifacts of a changing labor market, still give us signals that the US economy isn’t as bad as many want it to be at 4.5% Fed Funds Rate to validate their place in the commentariat.

Europe is getting a small reprieve with the extremely mild winter so far, pushing energy prices down, especially natural gas, for now.

The global recession talk is vastly overblown until something fundamentally breaks. Anyone looking at the end of the year book squaring in things like the Reverse Repo balance (+$300b in one week) is overthinking the problem. The banks are allowed to tailor their reserves to present whatever quarterly numbers they want. It’s been going on since the Bernanke Era.

As such, I see a kind of perfect storm for oil here. Russia will pull production off the market and shift exports from St. Petersburg (Urals grade) to Kosmino, near Vladivostok (ESPO grade), nabbing higher prices in the long run.

Arab OPEC can’t hit its production quotas as it is and China’s reopening its entire economy.

The Davos demanded ESG investment protocols have the oil industry anywhere from $600b to $1trillion underinvested in exploration and production and that number is rising.

Increased demand, tight supply, low replenishment investment and WAR. Even a moron or Joe Biden can see that $70 per barrel Brent is out of the question for any significant period of time.

9) Dow Jones 40,000+

As we enter 2023 the Dow Jones Industrials sit right around 33,000. It was a tumultuous 2022. After hitting a new all-time high a year ago at 36952.53 it was all downhill for most equity indices.

The stronger USD fueled a lot of capital reorganization, interest rates were finally forced higher by the Fed and incessant talk of recession kept everyone selling first and asking questions later.

But in this ‘pivot-obsessed,’ low pain environment, relief rally after relief rally was snuffed out until finally in Q4 the Dow made everyone stand up and take a little notice as to what was happening… flight to quality into tangible assets with deep liquidity pools.

The Dow lost 8.7% in 2022. The S&P 500? 15.8%. The NASDAQ? 27.7%

For all of the bitching gold bugs did in 2022, gold was up 1.6%

If we begin to move into the next stage of stagflation (#1) then the Dow will continue to outperform the broader US equity markets as well as major foreign equity markets.

2022 Foreign Performance:

German DAX in 2022: -9.2%

Euro Stoxxx 50: -7.2%

FTSE 100: 1.2%

Are those indexes sustainable given the economic outlook for Europe and the ECB following the Fed up the rate curve lest everyone ‘lose their religion’ in it? Or will the still weakly expanding US economy look more tasty to global investors and the hopeless Brits look insanely overvalued?

If we have another year like we did in 2022 where high inflation outpacing nominal growth drives tangible asset investment we should see an outperformance from the US vs. Europe as the currencies collapse and the ECB’s tools prove inadequate. Emerging Markets, depending on their proximity to China and the US may have banner years, especially those that underperformed in 2022.

Highlights & News

World food prices hit a record high in 2022.

China is trying to avoid holiday gatherings to combat covid.

Sales of fully electric vehicles almost doubled in 2022.

U.S. wages were up +4.6% annually. But was almost half of what inflation was.

Temps remain brutally cold in Russia, with lows of -40 degrees Celsius.

Other Markets

Crude oil up +1 to 74.78

Dow Jones down -120

Dollar Index down -0.706 to 102.94

Cotton up +0.54 to 86.22

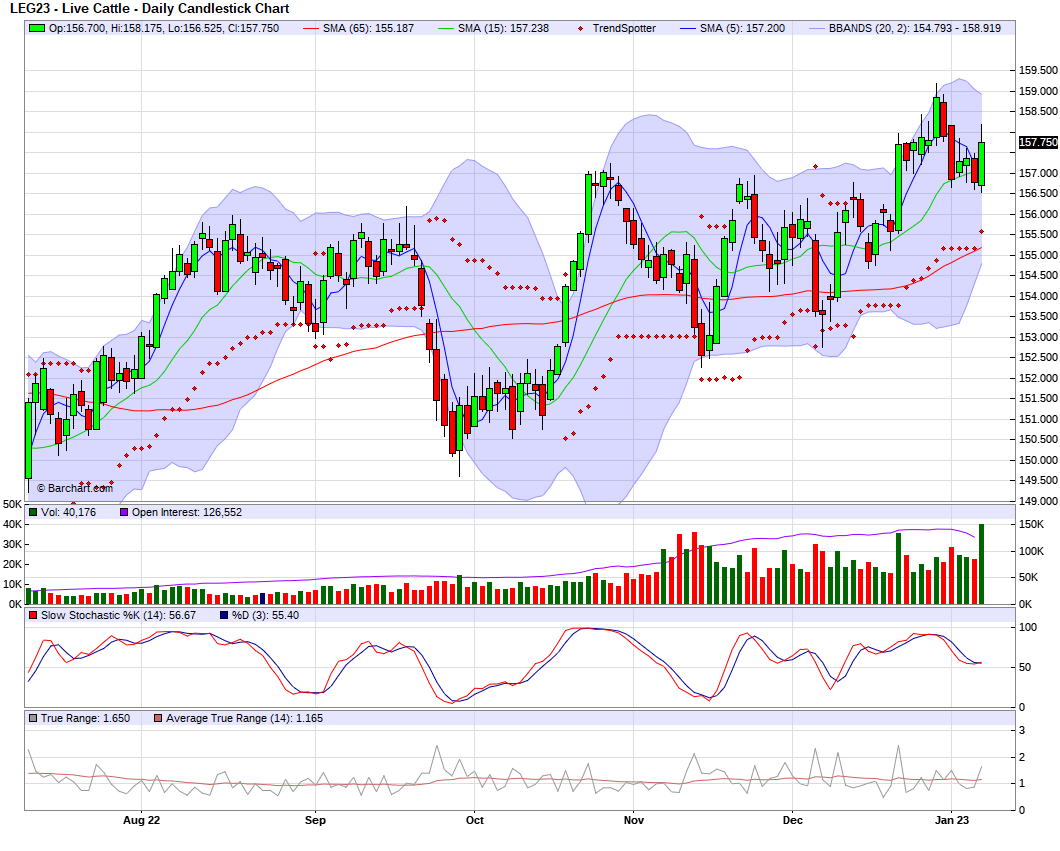

Livestock

Live Cattle up +0.975 to 157.750

Feeder Cattle up +0.650 to 186.300

Live Cattle

Feeder Cattle

South America Weather

Russia 24 Hour Forecast

Social Media

All credit to respectful owners

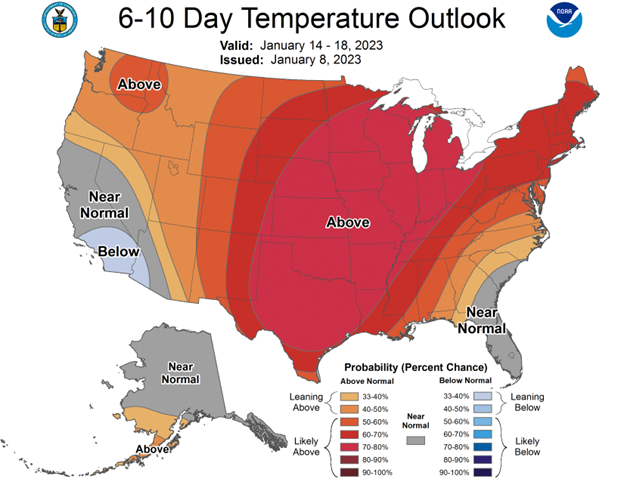

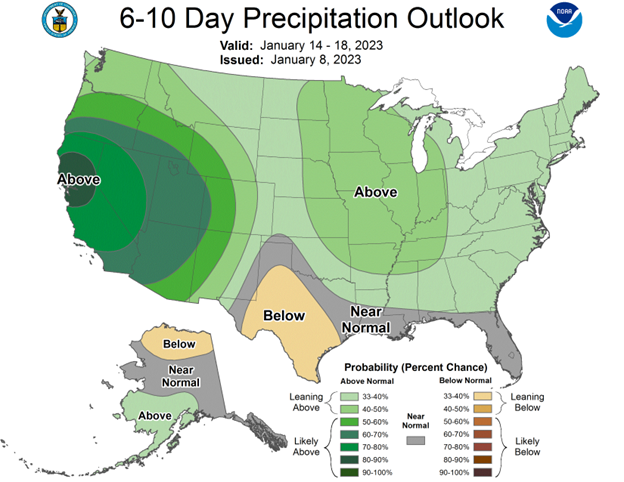

U.S. Weather

Source: National Weather Service