SOYBEANS & SOYOIL RALLY

MARKET UPDATE

By Sebastian Frost

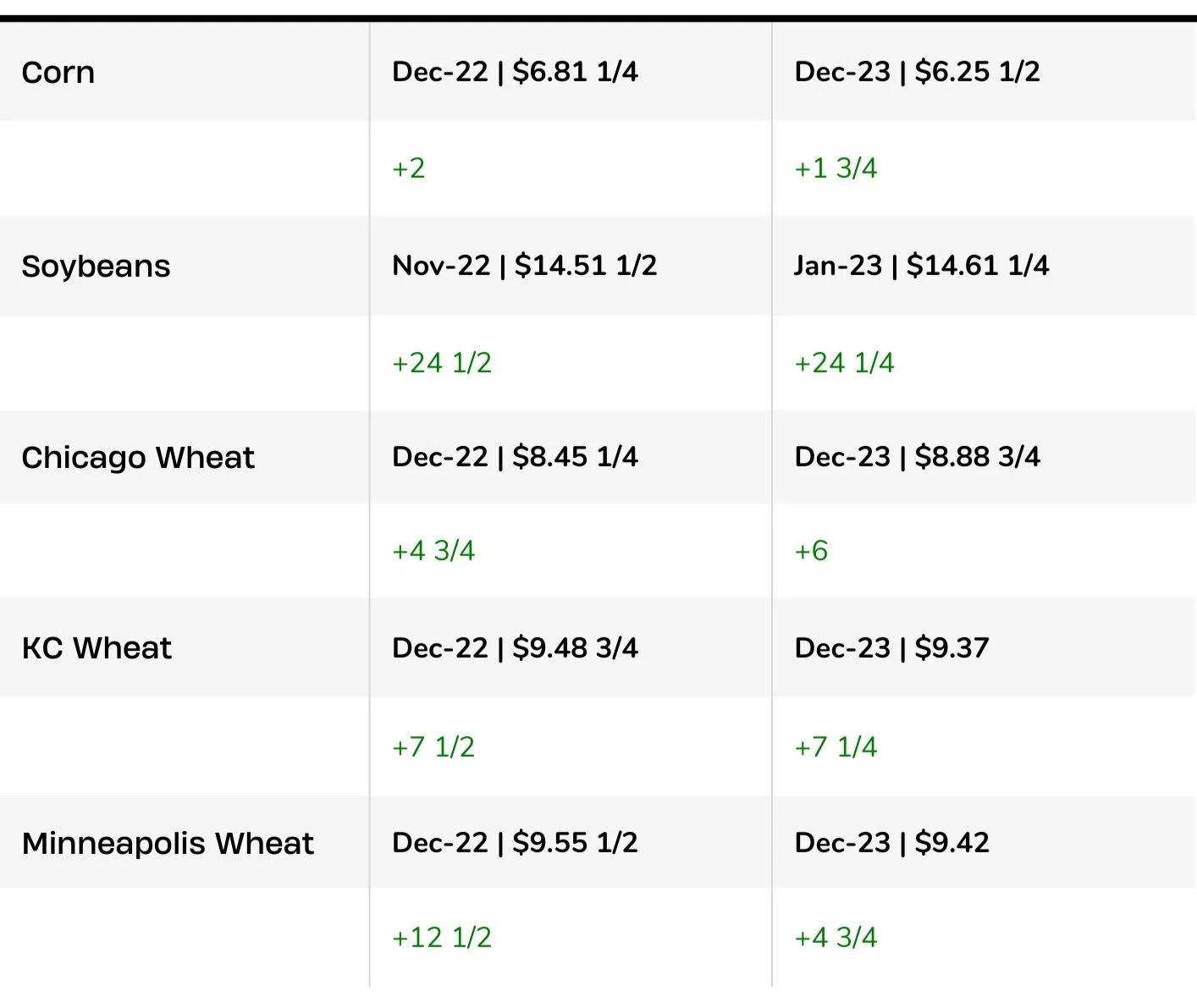

Futures Prices 11:00am CT

Overview

Grains higher today, led by a rally in soybeans. Soyoil also rallying an additional +2.5% following the stellar week its already had. Crude oil also very strong again today back over $90, now at its highest level in almost a month. The dollar weaker, now back down to where it was before it rallied Wednesday, adding additional support to the markets.

Today's Main Takeaways

Corn

Corn is following the markets this morning and is trading slightly higher. But for the most part just continues to trade back and forth in a very choppy range, continuing its pattern before the Russia/Ukraine news. Overnight we saw corn touch its 50-day moving average and bounce.

Corn continues to receive pressure from the underwhelming exports and poor demand. Taking a look at the recent export sales as an example. They came in at the lowest for a week we have seen since 2012. China is getting ready to start importing corn from Brazil which won't help us on the demand side. WE are also looking at the possibility of cuts in ethanol exports. However, the main focus will be next week's USDA Supply & Demand report set for November 9th.

The final yield still seems to be a pretty big debate. With the USDA lowering their estimate in their last go around. Bringing their estimate from 172.5 to 171.9 bushels per acre. But then on the other hand, we have recently seen some outside analysts actually increase their estimate. Such as StoneX who raised theirs up to 174.5 bpa as well as IHS raising theirs to 172.9 bpa, both higher than that of the current USDA. So ww will have to see what adjustments the USDA decides to make.

Crude oil very strong again today, trading over +$3 higher further giving support to the corn market. Crude oil is now at its highest level in over a month. A lot of the strength is coming from China saying they would be making changes to their zero covid policy.

Dec-22 (6 Month)

Soybeans

Soybeans very strong this morning, up over +20 cents adding on to the weekly gains we've already seen. Soybeans now well over that $14 resistance level we were talking about not all that long ago. Soybeans now almost at $14.50 with the +60 cent gains on the week (+4.50%).

The strength in soyoil has been a key factor in pushing soybeans higher as we've seen. As on Wednesday (Nov. 2) we saw soyoil rally 3% and hit the highest prices we've seen since June. Since then soyoil has continued to rally and push higher. Now up nearly +7% on the week. Currently up +1.80 (+2.40%) to over 77 today.

Exports have recently been somewhat beneficial to the soybean market. But this week's numbers came in on the disappointing side and lower end of the estimates. We will have to see whether or not we see any adjustments made to the export forecasts. Last month the USDA lowered its forecast by -40 million bushels. Given that they just lowered it in the last report, its not looking too entirely likely we see another one made here. As they will likely take a deeper look and digest everything longer before making any additional changes. Estimates for next weeks yield are expected to be unchanged at 49.8 bpa, with an estimate of 212 million bushel carryout, October was 200 million bushels.

Last month the USDA lowered its soybean yield estimate from 50.5 to 49.8 bushels per acre. Similar to corn, some outside analysts have begun to raise their estimates. With StoneX raising theirs to 50.9 bpa and IHS raising theirs to 50.3 bpa.

We also have rumors of China backing off their zero-covid policy, so we will have to see if this has any effects on Chinese demand.

If we want to see soybeans continue to push higher and break into the potential $14.80 or so range, we will more than likely need to see a lot more bullish headlines.

Likely the biggest factor going forward here for soybeans has to be South American weather, and whether they will see any problems arise due to weather complications.

Soymeal & Soyoil

Soymeal up +5.1 to 419.4

Soyoil up +1.83 to 77.12

Soybeans Nov-22 (6 Month)

Wheat

Wheat is now almost back to where it was just a week ago before the Russia suspension news hit the headlines sending wheat soaring higher. We are still roughly +10 or so cents higher than where we closed last week out, but have obviously gave up most of the gains made as Russia reagreed to the export deal. Wheat futures are currently up +6-12 cents this morning looking to end the week higher.

Taking a look at the export numbers. U.S. wheat exports had its best September in 9 years at 3+ MMT. However, we have to keep in mind that June and July were some of the worst we have ever seen. With 22/23 total sales still sitting at over 20 year lows.

The Russia and Ukraine situation still remains a mixed bag. One day its looking like Russia will renew the deal,t the next day headlines are saying they won't. In an update we saw this week, Russia said they can back out of the export deal anytime, but they will make sure that the grains flowing from Ukraine and Turkey remains unaffected and aren’t interrupted. We also saw Russia again making the complaint that Ukrainian wheat wasn't going to the poorer countries in much need. So there is still a chance Russia does not renew the grain export come the deadline on Nov19th, but we will just have to wait and see.

Globally, the excessive rain and flooding we are seeing over in Australia is expected to lead to some quality issues, potentially reducing the amount of wheat that's viable for humans to even eat. BAGE lowered their Argentina crop estimate due to the frost they received earlier this week.

Looking forward to next week's report, nobody is really looking for any major adjustments to be made. As those usually don't happen until January. Last month we saw yield lowered from 47.5 to 46.5 with acres being lowered down -2 million to 35.5 million. With production being lowered by-133 million bushels. With the fairly large adjustments we saw last month, we will have to see what the USDA does here. Especially given the global situations with Ukraine and Argentina etc. The average estimate for wheat carryout in next weeks report is 578 mbu, in October the USDA had 576 mbu.

So factors remain the same as they have been as of late. With the obvious Russia & Ukraine situation still a big potential factor to swing things. As well as global weather and Argentina. We still also have the recession fears and a strong U.S. being at play. Long term, there is still some potential for wheat, but we will have to wait and see how these other factors pan out.

Chicago Dec-22 (6 month)

KC Dec-22 (6 month)

MPLS Dec-22 (6 month)

Other Markets

Crude oil up +3.69 (+4.21%) to 91.58

Dow Jones down unchanged

Dollar Index down -1.5 (1.35%)

Cotton up up +4.09 to 87.09

News

Unemployment rose from 3.5% to 3.7%

Global outlook for palm oil remains uncertain. While covid policies weigh on Chinese demand.

Brazilian road blockades are affecting around 45% of the countries poultry and hog slaughter capacity.

Two unions rejected the proposed deal with U.S. railroads. While six approved it. All 12 unions must approve the contracts to prevent a strike.

Seven ships carrying Ukraine food leave Black Sea ports

Australian wheat crop faces potential downgrades with the flooding causing damage

BAGE cuts their Argentina wheat estimate to 14 MMT from 15.2 MMT

Livestock

Live Cattle up +0.050 to 152.00

Feeder Cattle up +1.000 to 180.425

Live Cattle (6 Month)

Feeder Cattle (6 month)

In Case You Missed It..

Read Sunday's weekly newsletter

Yesterday's grain market commentary

Social Media

All credit to respectful owners

Precipitation Forecast 2-Day

Weather

Source: National Weather Service