WHAT HAVE FUNDS ALREADY FACTORED IN?

WEEKLY GRAIN NEWSLETTER

Some not so fearless comments for www.dailymarketminute.com for our weekly newsletter for March 26th.

Funds vs fundamentals vs factored in

As we near next week’s big USDA acre and quarterly we ask our what are the funds thinking for grains, what are our fundamentals telling us, and what is already factored in.

Why has China been strong buyers of US corn followed by Xi being in Russia, which then leads to Russia making statements about halting wheat and sunflower exports, followed by ensuring that prices paid to farmers are high enough to cover costs. If you remember correctly just a few months ago we had leaders of Russia and Brazil make comments about needing to increase domestic stocks or carryovers to help their national food security issues.

So the way that I read it is that our biggest competitors for wheat, corn, and soybeans have publicized statements about needing to increase food security, now we have the biggest buyer in the world starting to buy US corn in a strong manner.

Last week’s export sales were the 3rd biggest week in the past 20 plus years. That is a big statement and shows how strong demand has changed in corn in just a few short weeks. If you remember in the March USDA Supply and Demand report we had another decrease in corn exports.

This week’s USDA report will give us an update on the fundamental outlook, but the bigger factor will be what is already factored in. Jon Scheve has a good write up on how important the report is which can be found here: https://www.wrightonthemarket.com/post/market-commentary-for-3-26-23?utm_campaign=4b050c92-68d4-4188-9470-2bb69963b713&utm_source=so&utm_medium=mail&cid=35b0e00f-a054-4b56-b772-27b0d83c8640

We will get more estimates as we get closer to Thursday’s report, but so far it appears that the market is pricing in more acres for both corn and beans. I would remind one that this is a producer survey and historically it tends to come in below expectations. There has been huge acre numbers being thrown out by some, but the market probably has priced in some big acres.

Here is a good write up from Pro-Farmer showing some of their thoughts on the acres.

The real question is what is factored in? Then more importantly than acres will be growing conditions and planting conditions that will either lead to more or less acres of various crops.

My bet is that we start our seasonal rally once we have our acre report behind us. It might take getting to the April Supply and Demand report which will be affected by our quarterly stocks report. If you remember our stocks for the January report came in well below estimates. But that led to the USDA simply dropping demand.

It doesn’t feel like that can happen again, as we have seen strong demand via exports for corn recently. And for soybeans we saw the export numbers cut in January only to see them increased in February and March.

Despite our markets getting beat up on price the past several months, we have tight fundamentals that don’t allow for a lot of room for more demand and they certainly don’t have wiggle room for a major 2023 production issue. Any increase in demand especially if met with production setbacks will only cause our prices to get carried away to the upside.

Commodities and grains will and always have been very volatile, with the ability to overdue price moves. We have over done the price move to the downside for new crop corn, wheat, beans, bean meal, sunflowers, and basically all grains. Can we now over do a bounce to much higher levels then needed is the qu estion?

Can we give the funds a headline that they want to stand behind? Do our fundamentals indicate that we should or could go much higher in prices? What is already priced or factored into our price prices and what isn’t priced into our present prices?

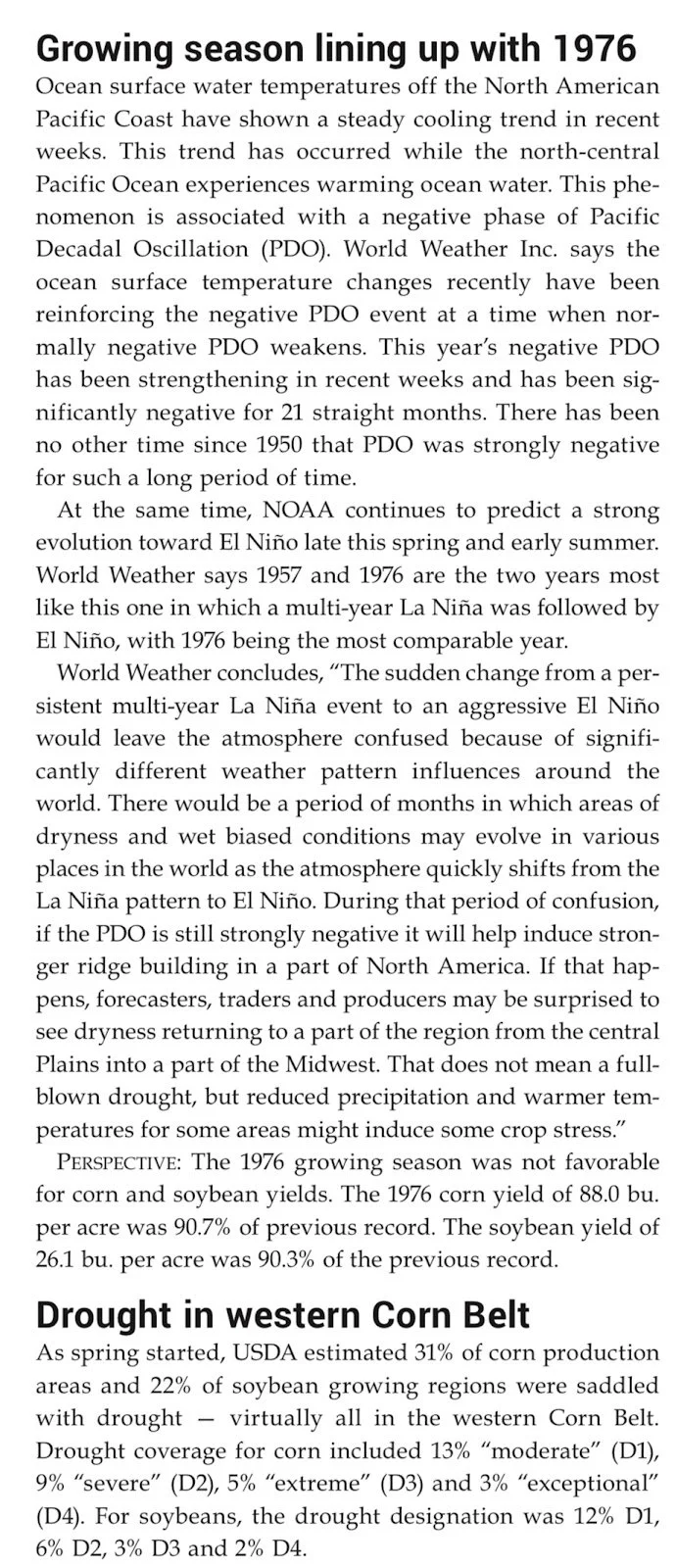

Weather

What will our weather be going forward? I have been saying for months that I think we have the possibility of a 2012 type drought hitting the corn belt in 2023.

Here is another write up on weather from ProFarmer, notice that they compare to a year that was around 10% below trend. 10% below trend line in 2023 puts corn yield in the low 160’s. What would that do to prices? Especially if the funds are short (like they presently are).

Here are some more weather comments from Farms.com Risk Management.

When we talk about factored in; one question that comes to mind is what part of the seasonality is already priced in?

Here is from Jason Britt on Twitter as he points out a seasonal trade that has worked well in the past.

Below is a recap on Friday from Farms.com Risk Management, notice he mentions the same seasonal trade.

Bottom Line

The bottom line is we feel that we have potential stories and headlines that have not been factored into our current price levels. Stories and headlines such as demand and production challenges that the funds haven’t priced properly. We feel there is still much more upside than downside and we believe that the break we have had in prices the past few months will help us go higher than we thought just a few months ago. We realize that the biggest risks are that Mother Nature allows perfect big crops to grow everywhere with no weather scares and fear of black swans as more banking issues develop and keep money out of the grains.

If you are managing a grain fund and look at the recent export sales to China, look at our balance sheet, and then get scared of a drought you would be getting very long in a hurry.

Charts

Corn 🌽

We got that break above the $6.37 and $6.40 we had been talking about, also closing above our 20-day moving average for the first time since February 21st. Next upside target is the $6.60 range and our 100 & 200-day moving averages just above.

Beans 🌱

Last week I mentioned we would likely go to test the $14 psychological support level and our upward trend line. We bounced just above those levels, hitting a low of $14.05. Bulls would like to see us break out of this short term downtrend we have created. We shouldn’t be too surprised though if we do eventually go back and test that bottom trend line, but bulls would like to hold above that line.

Chicago Wheat 🌾

Wheat again bounced off their recent lows and support of $6.55. Bulls would like to break past that bottom trendline, and myself would like a break past the $7.13 range to see higher prices and emerge out of this downtrend.

Crude 🛢

Crude showed some life after its massive downfall. But we still didn’t break out of the long term downtrend. I mentioned this a few times the past two weeks but I'm still not completely sold that the bottom is in just yet. Nearby support is where we bounced at the $65 range, with further support at $62 and $57.

Dollar 💵

Check Out Last Week's Updates

3/24/23 - Audio & Market Update

RUSSIA HALTING WHEAT & SUNFLOWER EXPORTS?

3/23/23 - Audio Commentary

CHINESE VS THE FUNDS

3/22/23 - Market Update

BEANS & WHEAT SELL OFF CONTINUES

3/21/23 - Market Update

BEANS & WHEAT CONTINUE TO DISAPPOINT

3/19/23 - Weekly Grain Newsletter